What would be the financial impact on your loved ones if you died? Would your loved ones struggle financially without your income? Though these questions about death and finances may be tough to consider, it’s important to answer them so you know your family will be taken care of if something happens to you.

In preparing for death, you and your loved ones should discuss what to do when someone dies. What will be the state of your finances after death? Do you have life insurance to protect your loved ones if something happens? To ensure you and your family are prepared, you may want to create and follow a financial checklist before death.

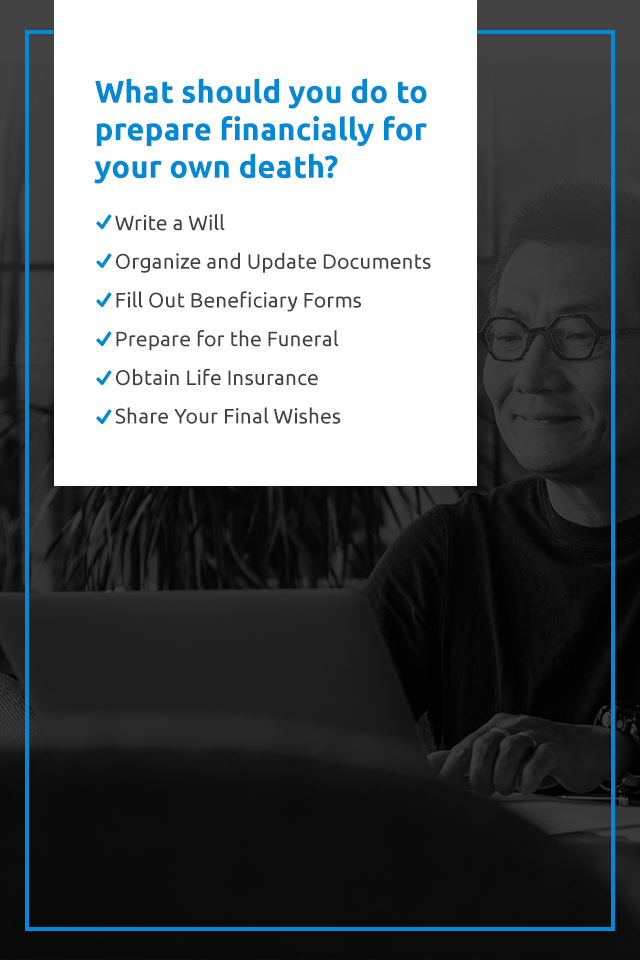

What should you do to prepare financially for your own death? Follow these steps to ensure your loved ones are taken care of financially after you die.

What do you want to happen to your assets and estate after you die? This is what a will is for — to declare who will be carrying out your wishes posthumously, who will receive which assets, who will care for your dependents or pets and any other details of your estate and life that will affect your surviving loved ones.

Who will receive your rental property? Who will you transfer your bank accounts to? Who will receive your retirement savings? These are all questions that can be answered in your will.

Ensure your will is secure but accessible to your loved ones in the event of your death. Without your will, your loved ones may struggle to access your assets, or they may lose control over how those assets are distributed. If it’s important to you that you control how your assets are distributed, then you should write a will.

A lack of a will could create tension among your family members, who are already stressed and grieving. To avoid putting an additional burden on their shoulders, be sure to draft a will that clearly names who you want to handle your estate and where you want your assets to go.

Review your will periodically and update it as needed. You can hire a financial planner or attorney if you need help with drafting your will.

Keep your documents with important information about items like your checking account or pension benefits organized, accessible and up to date for your surviving family members. Make a list of all of your online accounts and user names so your loved ones know what accounts to look for. Online storage sites provide a safe place to list your accounts, or you can compile all of that information on a document that you then store in a secure place. In this document, you should include:

Besides your financial assets, you should also keep an organized and updated record of your financial liabilities. List all of your debts, such as your mortgage, car note and credit card debt. Include your tax-related data and documents and a list of people to contact after your death as well. Be sure to also include the contact information of anyone you want to be contacted after your death so that the task is easier for your loved ones.

On top of keeping all of this information updated and well-organized, make sure it’s also accessible to your family members. If none of your loved ones know where to look for your documents, they won’t be able to use them.

Sometimes if we’ve already drafted a will, we forget or neglect to also fill out our beneficiary forms. Ensure that you have not only filled out your beneficiary forms before your passing but also that you’ve filled them out correctly. Even with a will, some state and federal laws can interfere with your wishes if you haven’t properly completed the required paperwork. By filling out any necessary beneficiary forms, you’re ensuring that you and your loved ones are financially prepared for your death.

Funerals aren’t cheap. In fact, they can be prohibitively expensive for families who are already struggling financially. Your family will need money to cover the casket, the service, the burial or cremation, the plot of land, the gravestone and more. To alleviate your loved ones of this financial burden, prepare financially for your funeral.

Do your research to determine roughly what a funeral might cost, keeping in mind what sort of service you want and whether you wish to be buried or cremated. You can prepay for the costs, add the amount you expect to your life insurance policy or save money in an account for the funeral and its associated expenses.

Life insurance provides your loved ones with financial support in a time when they may really need it, especially if they’ve been depending on you financially, and your death was unexpected.

You can obtain a permanent life insurance policy or a term life insurance policy. A permanent life insurance policy is more expensive, but as long as you’re making the payments on time, it will last your entire life and pay out to your family when you die. The policy also provides cash value, so a portion of your premium is invested for you, and you can use this money if needed.

A term life insurance policy is for a set amount of time, and your beneficiaries will receive the policy amount if you die while the policy is active. This type of life insurance policy is cheaper, but it won’t pay out if the policy expires before you die.

Include information about your carrier and policy number in your documents so that your loved ones have access to this information in the event of your death.

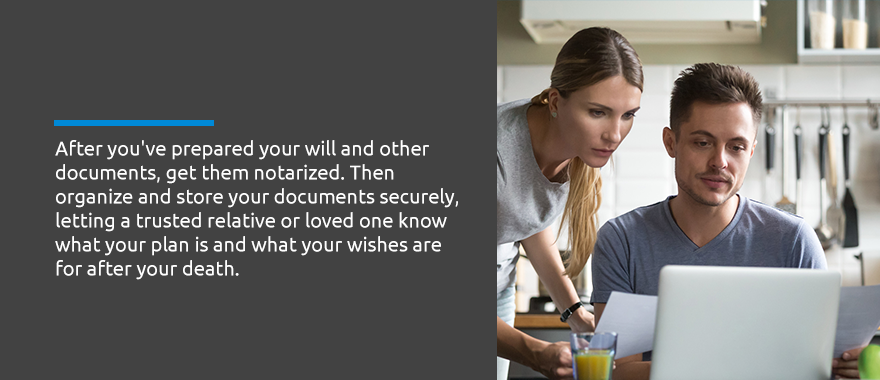

After you’ve prepared your will and other documents, get them notarized. Then organize and store your documents securely, letting a trusted relative or loved one know what your plan is and what your wishes are for after your death. If you communicate your preferences to your loved ones, they’ll know exactly what you want, and they won’t have to stress about making decisions on your behalf or worry about what you would’ve wanted.

We might not like to think about money when someone dies, but even though it’s a tough conversation to have, everyone involved will be better off after that discussion takes place. Your loved ones will feel more comfortable executing your final wishes knowing that they’re doing exactly what you said you wanted, and you won’t have to worry about adding stress to your loved ones’ lives after your death.

Be sure your loved ones follow these steps in preparing for their own deaths as well.

What should you do to prepare financially for the death of a loved one? In preparing for the death of a loved one, follow these steps:

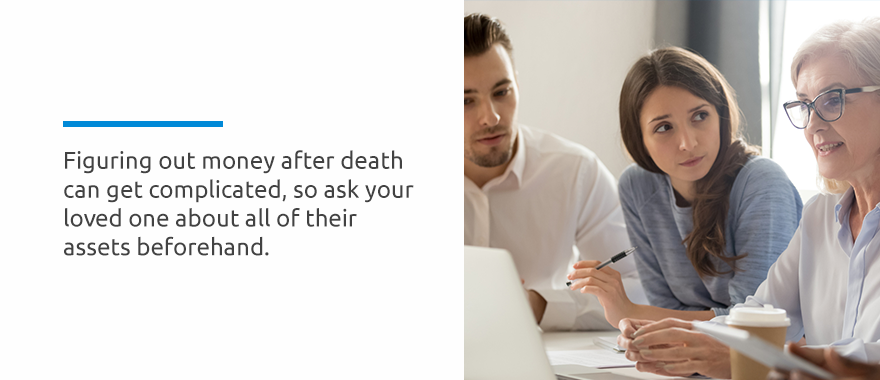

Figuring out money after death can get complicated, so ask your loved one about all of their assets beforehand. Ask what assets they own and where those assets are held. You should also find out this information about all of their liabilities.

Ask your loved one where they stored their wills, tax records, trusts and other financial plans. You should also know any user names and passwords for accounts that you’ll want access to, such as accounts that contain family photos.

If your loved one has an asset in their name, check that these assets offer “spousal transfer,” which transfers the rights to that asset, like a checking account, to you after your spouse dies. A bank can freeze an account if the account holder dies, so know how these assets are titled before you’re faced with this dilemma.

Some credit cards close automatically following the death of the owner of the card, so if your loved one had set up automatic payments through their credit card, you may need to set up a new payment method.

If you are a co-signer on a loan with your loved one or the loan is solely in their name, find out how those loans are handled following your loved one’s death. The laws for car loans and mortgages vary by state, so be sure to do your research.

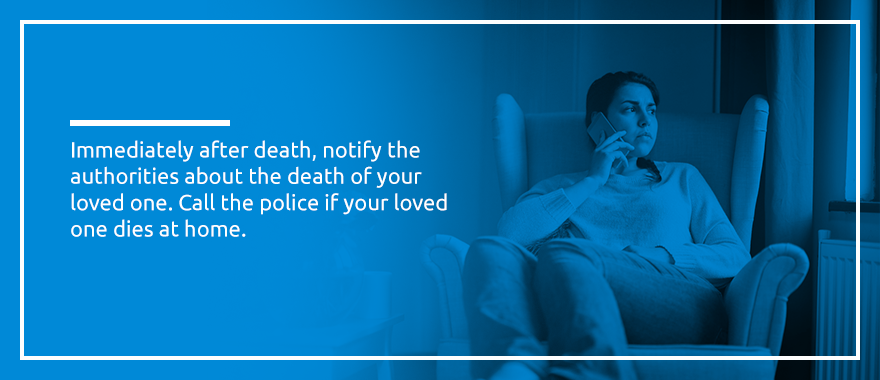

Immediately after death, notify the authorities about the death of your loved one. Call the police if your loved one dies at home. If your loved one has been receiving hospice care, they’ll inform you about how to proceed when death occurs.

You should also be thinking about organ donation and autopsy, along with how the body will be cared for and informing other loved ones about the death.

You’ll also want to look for a will or letter of instructions after the death of your loved one. Your loved one may have left behind instructions for their funeral or other services, so you can use this to guide you in honoring them after death. Look in the loved one’s home and ask relatives and friends if they have any information.

In the days after the death of your loved one, you’ll also want to complete the following tasks:

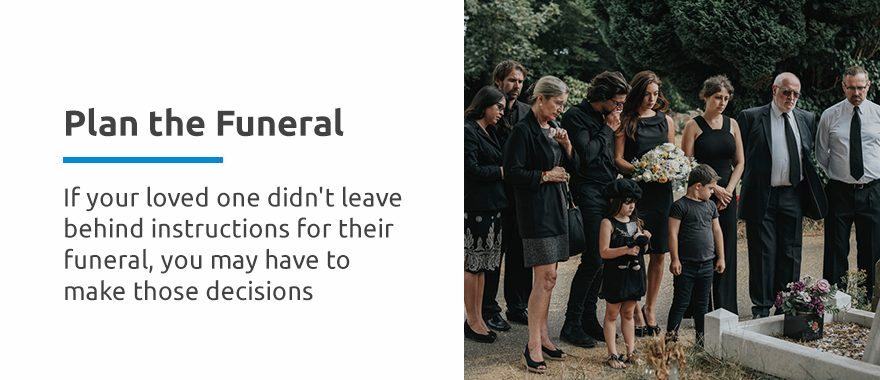

If your loved one didn’t leave behind instructions for their funeral, you may have to make those decisions yourself. In some states, you may be able to hold a burial without using a funeral home, but in other states, you’re required to use a funeral home. Research your state laws, and then select the facility you would like to use.

You also will want to determine whether the body will be buried, cremated, placed in a vault or donated.

Of course, you’ll also need to consider how the services will be paid for. Did your loved one leave cash behind earmarked for their funeral? Does the deceased have a joint account with a surviving spouse? You may be able to utilize veteran’s benefits, Social Security benefits or burial trusts under Medicaid. The funeral home may allow you to pay in installments, or your loved one may have a life insurance policy that can cover their funeral expenses.

The obituary is the notice of your loved one’s death that will be printed in the newspaper. You can receive help in writing the obituary from the funeral director or counselor, who will also send the obituary to the local newspapers on your behalf. You’ll be asked for information on your loved one, so be prepared with the information you want included in the obituary.

After the funeral is over, there’s still more to be done over the next few days and weeks. One of those tasks is locating and reading through your loved one’s will or letters of instruction. The will should contain information about settling the estate, and submitting this document is usually a time-sensitive issue.

The letters of instruction should inform you and your family members about how to divide your loved one’s belongings and what should be done with their assets. Though letters of instruction aren’t legally binding, people typically like to keep their deceased loved one’s final wishes in mind as they move forward.

You don’t need just one death certificate after your loved one passes. Odds are, you’ll need many — sometimes as much as 20 or more. You’ll need a death certificate for each place you apply to for death benefits, such as the Social Security Administration, a life insurance company and the Veterans Administration. You’ll also need death certificates for every bank or investment account your loved one held.

While some institutions accept copies, others require original death certificates. If you need to order more, this can delay progress, so order plenty upfront so you don’t have to worry about delays while you’re getting your loved one’s estate settled.

After your loved one passes, you may need to change security codes on their home alarm system, their phone voicemail and more. You should be able to contact the companies maintaining the alarm or phone, provide them with identifying information about your loved one and change the security codes so you can access their home or voicemail messages.

If your loved one didn’t prepare their finances before their death, you could be left searching for their assets. So, where should you look, and what should you look for?

Assets you should be looking for include:

To locate your loved one’s assets, search through:

If you’re unable to find anything, you may be able to contact a service that can locate lost property or check with your loved one’s employer or a professional organization they belonged to.

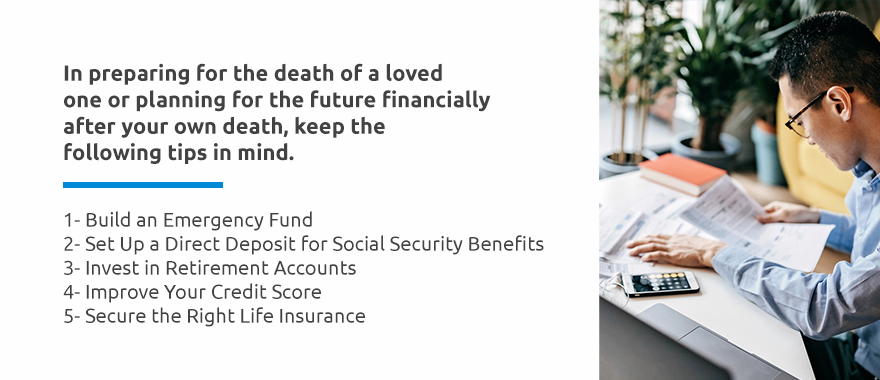

How can you prepare your finances so that your family is taken care of if you die? How can you prepare your finances for the possibility that your spouse passes away unexpectedly? In preparing for the death of a loved one or planning for the future financially after your own death, keep the following tips in mind.

An emergency fund can cover expenses that come up that you didn’t expect, like a hospital bill or a job loss. You and your spouse can build a joint emergency fund, or you each can have your own emergency savings. At a minimum, your emergency fund should be able to cover three months of expenses. Even better, you can save an emergency fund that would cover 6 months to 9 months of expenses.

To prevent your Social Security benefits from getting lost or delayed, you can set up a direct deposit for your benefits into your bank account.

If your employer offers a 401K or pension plan, you can contribute to these accounts to save for your retirement. You can also invest in retirement accounts outside of your employer-sponsored plans, such as an IRA.

Establishing credit in your name and improving your credit score can help you financially. Pay your bills on time, pay off your credit card balance every month and keep your credit utilization rate low to increase your credit score.

One of the most important steps in preparing for your family’s financial future is securing the right life insurance policy. Your life insurance benefit after death can help reduce or eliminate your family’s financial burden after you’re gone.

If you’re the primary or sole breadwinner in your family and you have a spouse and children relying on your income, you should have life insurance. If you’re a stay-at-home parent who saves your family a significant amount of money by eliminating child care costs and shouldering the majority of the household duties, you should have life insurance.

Life insurance can cover your funeral costs, pay for professional care for your elderly dependent, pay off your debts and provide financial protection for your spouse, children, business partner or employees. To avoid leaving your loved ones with a financial burden after your death, obtaining life insurance is key.

For quality, affordable life insurance, contact us at David Pope Insurance Services, LLC today.