Life insurance is essential for protecting your family’s financial future and preparing for the unexpected. Similar to other financial planning practices, you should review and adjust your life insurance policy regularly to reflect the current circumstances of your life. It is important to understand your coverage and when to make changes with any insurance. You can avoid lapses in protection or overspending with a strong comprehension of your policy.

Part of getting the most of your life insurance is knowing when to review it. Certain life changes call for a policy update. Being proactive about making these updates will give you a sense of confidence in the face of uncertainty.

It is best to review your life insurance policy every year, even when you feel your life circumstances have not changed. Revisiting your policy allows you to make alterations to reflect your and your loved one’s current needs. The following are important reasons for reviewing your life insurance policy.

As you review your policy and its coverage, it’s a good time to compare it with other options. The following are common types of life insurance:

Another option for a person looking for the benefits of a life insurance policy without needing to meet all the qualifications is annuities. Annuities are a form of investment contract to cover a person’s living expenses if they live longer than their financial means can accommodate. In addition, a person’s beneficiary will receive the death benefit when the policyholder dies like traditional life insurance policies.

It is beneficial to understand each type so that you and your insurance agent identify the best option for your personal needs.

Along with comparing your coverage to other policies, it is also necessary to revisit your premium costs. By reviewing your costs regularly, you can ensure your expenses are where they are supposed to be and avoid overpaying.

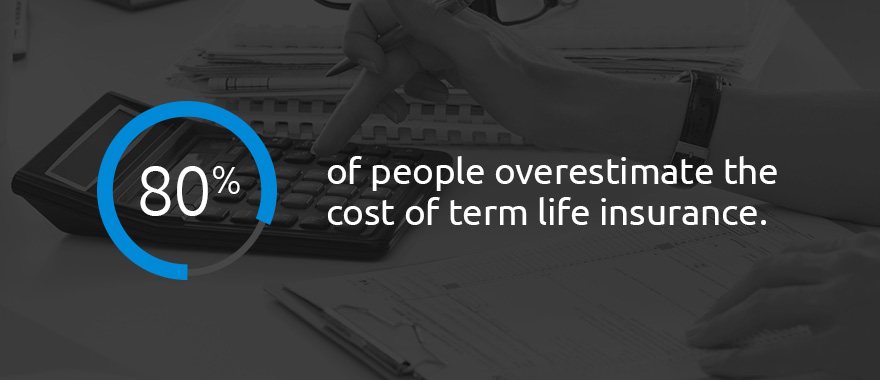

Most people — 80% — overestimate the cost of term life insurance. Reviewing it often allows you to see exactly what you need to pay for the coverage you want.

When reevaluating your life insurance policy, it is crucial to plan ahead and ensure your beneficiaries are adequately covered. You do not want to find yourself underinsured. After all, the purpose of life insurance is to benefit your dependents financially when you pass, providing them the monetary support they may need without you.

In addition to an annual insurance review, there are other instances when you should revise your policy. The following are different life changes that call for a life insurance update.

Getting married is exciting! If you recently tied the knot, you may have lots on your mind. Remember to update your life insurance policy to include beneficiary coverage for your spouse in case something were to happen to you.

It is especially important to review your policy if you are getting remarried, as your former spouse may be entitled to insurance money rather than your current partner.

Amid a divorce, it is easy to overlook your life insurance as you divide your assets and come to a child custody agreement. But, similar to getting married, you will want to review your life insurance policy if you are going through a divorce. This review allows you to make any changes regarding your beneficiaries. Going over your policy will ensure your children are covered and that you’ve removed your ex-spouse if you want.

Welcoming a new baby into your family is a necessary time to revisit your life insurance policy. While it can be hard to consider what your baby’s life would be like if you were to pass away, you must take the proper precautions to ensure your child is well cared for.

An insurance policy can provide financial security for your newborn and cover costs for everything from food and clothing to diapers and doctor’s appointments.

Reviewing your policy can help you set your child up for success in your absence.

When your children grow older and move out, your finances change. As your children become less financially dependent on you, you’ll want to revisit your life insurance coverage. Make adjustments that will secure your child’s future and allow them to continue at the same standard of living if you were to pass away.

If your children are financially well off, you may even choose to distribute your benefits to other areas of your policy.

Perhaps you recently closed on a new home. Congratulations! This is an excellent time to consider how this new home will be taken care of if the worst were to happen to you as the primary provider. It is crucial to revisit your life insurance policy when buying property so you can ensure your beneficiaries can adequately cover the costs if you die.

If buying a new house meant taking on a new mortgage, you’ll want to review your life insurance policy and ensure your loved ones can pay your mortgage in full if you were to pass away before paying it off.

By being proactive about changing your policy, you can save your loved ones a lot of financial strain after you are gone.

You put your house on the market, and someone put in an offer. Now you have to reassess your financials going into the future. While looking for a new home and selling the old one, it can be easy to overlook the need to verify your life insurance policy details. Be sure you keep your address and other personal information up to date.

Depending on the value of your old home and where you plan to go next, you may need to evaluate your coverage and potentially make some policy changes as well.

Starting a new business is exciting! It can also be very expensive and complicated. Whether your company has a storefront or operates online, you should evaluate your life insurance policy early in your entrepreneurial process.

Many business owners choose to take out a loan when starting their new venture. If you have a loan, you’ll want to ensure your life insurance policy is enough to cover any costs if you pass away and leave the business to family or close ones.

If your parents are moving into an assisted living facility or need additional care, this could result in some financial changes for you. It is critical to revisit your life insurance policy and make necessary changes when caring for your elderly parents, as you may need additional coverage.

You should review your policy after taking on any financial burden to ensure you’ve met your changing needs and have added security if something were to happen.

Your life insurance policy should reflect your lifestyle. If you had a recent health change, this could factor into your premium, so it is important to revisit your coverage and make any necessary modifications. The following are examples of health changes that would require a policy revisit:

Whether these are positive changes or not, they can impact your needs and preferences. Make sure to note any health changes at your next meeting with your insurance agent.

It is necessary to consider how your financials are affected when changing jobs. You may be making more or less money than in your previous position. Either way, you will need to readdress your life insurance policy and make changes to reflect your current income.

If you have accumulated some debt over the past year, you should consider meeting with an insurance agent. Whether you have new loans or medical bills, adding new debt can impact your beneficiaries if you were to pass away.

When you are discussing your policy, consider creating a monthly budget as well. The more accurate your finances are when you die, the easier the monetary transition is for those left behind.

When a loved one passes away, you may receive money in the form of inheritance. In some cases, you may get a small check. In others, the inheritance money is enough to change your entire lifestyle completely.

It is good to perform life insurance policy reviews and make modifications to reflect your inheritance money in either situation, but it’s essential if you come into a large lump sum. Your beneficiaries will be thankful.

When you have experienced the death of a loved one, it is important to address this change. If the deceased were one of your beneficiaries, you would want to update your coverage. If the loved one’s passing has impacted you financially, this may also call for a policy review.

Retirement is an exciting time. As you look forward to this change of pace, you will want to consider how your life insurance policy may need to change too. As you become older, it is vital to understand your finances clearly. This knowledge allows you to live comfortably in your later years and makes it easier on your family after your death.

It can be very exciting when your children start families of their own. As children are born, some grandparents choose to update their insurance policy to reflect this life change.

The addition of a new baby is a good time to reexamine your coverage, whether you want to add your grandchild as a beneficiary or increase the amount your policy gives to your children.

Beyond life changes, there are other reasons for a life insurance policy review. You should schedule a meeting with your insurance agent to go over the following annually:

The accuracy of your life insurance policy matters. Reviewing your information regularly allows you to feel confident in your coverage and find peace of mind.

To make the most of your life insurance policy, you should revisit it regularly. Your coverage should reflect your current lifestyle and needs. Committing to reviewing it at least once a year and during any significant life changes is essential for finding the right policy for you.

David Pope Insurance is an insurance provider located in Union, Missouri. We are family-owned and have over 20 years of experience in a full range of insurance services. Our team can help you navigate your life insurance policy and find the right fit for you and your loved ones.

If you’re interested in learning more, contact us today!