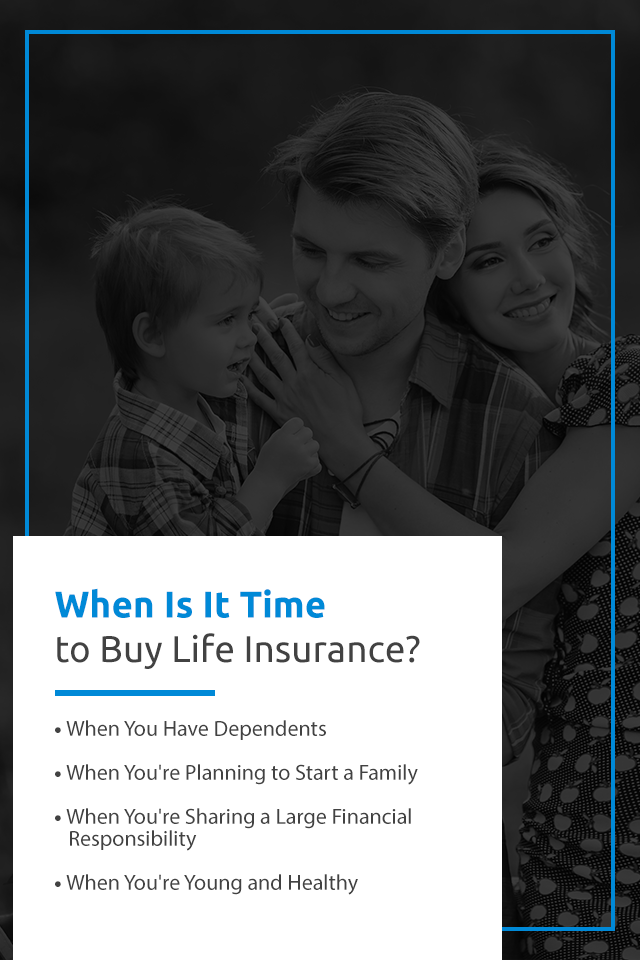

The simplest answer to this question is that your family needs you to have life insurance if they depend on your income. This generally refers to dependents, mainly your children, but can also refer to a spouse or parents who need to pay off debt.

If you’re in your twenties, single and childless, maybe you don’t need life insurance right now. But do you want marriage and a family someday? If so, keep reading. Are you married with children and don’t have life insurance? If so, definitely keep reading.

You may be asking yourself, when do I need life insurance? Do I need life insurance in my 20s? In reality, your decision about when it’s the best time for you to buy life insurance doesn’t have anything to do with age. Though your age may play a role in the amount of coverage you need, other factors will play the most significant roles in your decision.

Simply, when someone else is depending on your income, that’s the time to buy life insurance.

28 and single? You don’t need life insurance. 28 and married to a stay-at-home parent? You need life insurance. If you’re 28 and married, both you and your spouse work and you don’t have children, you may not need life insurance just yet. But you’ll want to start looking into it.

Another good rule of thumb? If you are starting a family, it’s time to buy life insurance. Life insurance will help your family to support themselves if you die and are no longer able to provide for them, so if you have dependents, obtaining life insurance is crucial.

You may even want to start planning for your life insurance before the birth of your first child. If you’re married and want to have children in the future, you and your spouse may decide to take out life insurance policies for each other. This applies even if you’re both working, as many couples rely on both incomes to cover monthly expenses. If either of the spouses would not be able to provide for the family on their own, life insurance is essential.

Even if you don’t have children, you may still want to obtain life insurance due to other special circumstances. If you have a parent who has cosigned for your mortgage or a sizable student loan, you may want to secure a life insurance policy that could cover their share of the loan if something were to happen to you.

You don’t need a huge amount of insurance in this case. You need only enough to cover the loan’s outstanding balance. If you have a cosigner who is legally responsible for your debt after you die, you want to make sure they are protected.

Buying life insurance while you’re younger provides an advantage since life insurance becomes more expensive as you get older. Worse, you may not be able to get life insurance at all if you develop a medical condition. If you’re young and healthy, it may be the best financial option for you to purchase life insurance now if you anticipate needing it in the future. Plan on getting married someday? Plan on having kids someday? Now may be the best time to buy life insurance.

Buying life insurance is a lot like saving for retirement — the longer you delay, the greater the economic impact. The younger you purchase life insurance, the better. With every year that passes, the policy grows more and more expensive. You also miss out on the years that your life insurance cash values could be growing tax-deferred. The longer the policy can accumulate, the greater the value, even with a fixed insurance cost for the entire policy term. If you hold your policy long enough, you can use cash values for a downpayment on a home or to supplement retirement income.

The right time to purchase life insurance varies from person to person. The best time for you to purchase life insurance depends on your age, family situation, life goals and whether you have dependents relying on your income. For many Americans, however, the ideal time to purchase life insurance is while you’re still young and healthy and can qualify for a low premium.

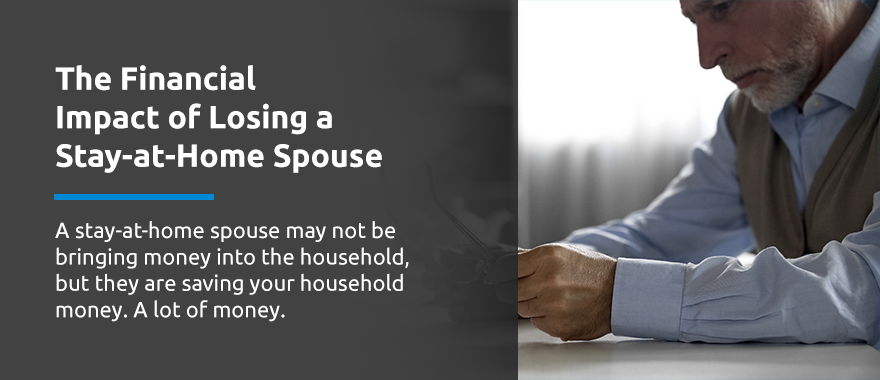

Many of us have heard the misconception that the primary breadwinner is the only person in a household who needs life insurance. In truth, however, a stay-at-home spouse is contributing a lot of work to a household — they just aren’t being compensated for it monetarily. If a stay-at-home spouse dies, someone else will need to do that work. And the services that a stay-at-home spouse provides for free are now going to cost you.

A stay-at-home spouse may not be bringing money into the household, but they are saving your household money. A lot of money. So when a stay-at-home spouse passes away, your household takes a significant financial hit.

Imagine the combined costs of childcare, housekeeping, cooking, financial management and the other duties your stay-at-home spouse provides to keep your household running. You may have to hire professionals to handle these responsibilities.

The cost of childcare alone can be exorbitant in America. The average yearly cost of childcare in the nation is around $9,000. This number can be higher or lower depending on the age of the child and the program type. For example, center-based care for an infant tends to be more expensive than home-based care for a four-year-old.

For many parents, childcare is unaffordable. For married couples, 11% of their income goes toward childcare. For single parents, the ratio is even higher, with a whopping 37% of their income going toward childcare alone. These numbers are quite a bit higher than the recommended 7% set by the Department of Health and Human Services. Can you afford to put 37% of your income toward childcare if your stay-at-home spouse passes away?

If you want to calculate how much it might cost financially to replace a stay-at-home spouse, you can use a wage comparable to each task and then multiply that rate by the number of hours spent on each task.

To protect your family if a death does occur, you can take out a life insurance policy payout that acts as a safety net for your household. Your beneficiaries can use the policy for various needs, including day-to-day living expenses, funeral costs and future planning. Term life insurance can be extremely affordable, making an excellent and viable option for many families.

If you’ve decided the stay-at-home dad or stay-at-home mom in your family should obtain life insurance, your next question may be: what’s the right amount of coverage? A stay-at-home spouse may want to secure an amount of coverage that is equal to the amount of life insurance held by the working spouse.

Coverage is limited to each individual’s financial situation, and quantifying a stay-at-home parent’s contribution to a household can be tricky. Here, the assumption is that both spouses are contributing to their household equally, which means you may both qualify for the same amount.

Decide together what amount of coverage will bring you the peace of mind you need, knowing that your loved ones are protected.

If you have kids, your life insurance policy has to provide not only for your spouse but for your children, too. Because incomes and expenses vary from parent to parent, life insurance needs will vary as well. So here’s how you determine what your life insurance needs are if you have kids, whether you’re a new or expecting parent, a parent with teens or an empty-nester.

While there are several types of life insurance, term life insurance tends to be the right choice for the majority of people. Term life insurance is life insurance that lasts a certain number of years before it expires.

Life insurance exists to cover your household’s expenses and replace your income. The cost of your expenses will influence the amount of life insurance you’ll want. Your life insurance amount should be enough to cover your expenses for a certain amount of time, ideally until your kids reach adulthood and move out, until the mortgage is paid off or possibly even longer. You may want to have a life insurance policy that covers everyday spending, the mortgage, funeral expenses and long-term care expenses.

As a new or expecting parent, how much should you leave behind for your dependents to provide for them? You’ll want to factor in the usual day-to-day expenses, such as food, diapers, formula, clothes and mortgage or rent, along with larger expenses, such as childcare, summer camps, health insurance and possibly tuition for a private school. If you’d like to help your child pay for a college education, you’ll want to factor that in as well. Depending on your cost of living, raising a child to adulthood could cost hundreds of thousands of dollars. Keep that in mind when you’re determining the appropriate amount of life insurance to cover you.

If you’re planning to get pregnant, the best time to purchase life insurance is before you become pregnant. This ensures that you’ll be covered if something were to happen during childbirth. If you’re already pregnant, you’ll either want to apply during your first trimester or a few months after you’ve given birth. Since life insurance rates factor in your health, any temporary symptoms from pregnancy, such as gestational diabetes or weight gain, will be considered when determining your rate.

Once kids are older, parents tend to still have the same expenses, but they also tend to have more assets. Maybe your home is paid off, or you have retirement savings, or you make more money than you did when your kids were younger. Similarly to parents with younger children or babies, you’ll want to calculate how much money will be needed to pay for the household expenses and replace your income until your kids leave home.

If you plan on helping your children with college, you’ll want to calculate how much you could reasonably put toward savings for college every month or every year and what your goals are. Fortunately, for teenagers, you need coverage only for about five or 10 years.

After your kids have moved out, you can turn the focus of your life insurance back toward you. How much coverage you’ll need depends on your expenses and your age, whether retirement is right around the corner or you still have a couple more decades to go.

Even when your kids leave home, you’ll still have your spouse depending on you. If you have a retirement savings goal, you want to make sure your spouse is set up for retirement by purchasing a life insurance policy. If your goal as a couple is to retire at 65, but you die at 55, that leaves your spouse with another decade before retirement. Life insurance can help meet your spouse’s needs during that gap.

Keep in mind that sometimes an empty nest isn’t always truly empty or doesn’t stay empty forever. Sometimes, children move back home after graduating from college, or you may find yourself with dependents who aren’t your children, such as older relatives or aging parents.

You likely won’t need as much coverage, but the coverage you have will allow you to feel more secure in your golden years.

Now that you know when to buy life insurance, how do you decide what type of life insurance is best for you? First, you’ll decide between the two types of life insurance: permanent and term.

Permanent life insurance combines a savings or investment account with a death benefit. This policy covers you for your entire life. Depending on your policy, your premiums may be fixed or not. They’re also based on your medical history and health.

Term life insurance covers you for only a set number of years and provides a death benefit. Your annual premiums are fixed and based on your life expectancy and health at the time that you apply.

For most people, term life insurance is the better option. Term life insurance is more affordable than permanent life insurance, even for the same amount of coverage. While a permanent life insurance policy does accumulate cash value through an investment or savings component that term policies don’t have, you’ll pay a larger premium for this feature. Your premium will also be higher because your policy is guaranteed to pay out someday, whereas a term policy may expire before that.

By spending less on term life insurance, you can invest or save the money you would’ve otherwise been spending on permanent life insurance. You also won’t have to borrow against your policy, which would diminish its value and defeat the purpose of having life insurance in the first place.

If you’re single and don’t have anyone relying on you financially, then you may not need life insurance. Generally, your death won’t have a significant financial impact on your loved ones. You may, however, want to consider purchasing an inexpensive, small policy that would cover your funeral costs, especially if your parents or immediate family don’t have the money to fund funeral and burial costs.

If you’ve recently gotten married and you’re young and healthy, you may want to go ahead and purchase life insurance. Major life events like buying a home and having kids typically necessitate purchasing life insurance, and the younger and healthier you are when you buy, the cheaper your policy will be. If your new spouse depends on you financially, you’ll want to have life insurance to keep them protected if anything happened to you.

If you wait until you’re older, the premium for the same amount of coverage will grow more expensive, and if you experience a decline in health during that time, you may not even be able to get insured.

Buying a home is an exciting time in your life. After you purchase your home and acquire a mortgage, you may begin receiving solicitations for mortgage protection insurance or mortgage life insurance. For most people, mortgage protection insurance isn’t necessary, and term life insurance will still protect your household if the primary breadwinner passes away. Term life insurance should cover your living expenses so that the surviving spouse isn’t left behind with a mortgage they can’t afford.

For many people, the most important time for them to have life insurance is when their children are depending on them financially. If you’re expecting a child and don’t already have life insurance, now is the time to get it. If one spouse passes away, the surviving spouse will have the sole responsibility of caring for and providing for the children.

A substantial policy size is recommended for this stage in your life, as you’ll want coverage for at least the first 18 years of your child’s life. The policy should cover typical child-rearing expenses, along with your usual household expenses. Some parents also want to be able to contribute to or pay for a child’s college tuition with their policy. You want a policy large enough to allow your family to maintain their current standard of living. This may mean purchasing more coverage if you already have a policy.

Depending on when you purchased your life insurance, your term policy may run out by the time you retire. Buying life insurance when you’re older, however, can be extremely expensive.

Is life insurance really required if you’re about to retire? If you’ve planned for retirement and built up a nest egg, you probably don’t need life insurance at this age, as your nest egg should be able to provide for your surviving spouse. You may also have already paid off your mortgage, and your children may no longer be depending on you. If this is the case, the day-to-day expenses in your household are likely lower, and your spouse shouldn’t be overwhelmed with financial burdens if you pass away.

Having the appropriate coverage is essential when it comes to protecting your loved ones. That’s what makes working with a trustworthy insurance company so valuable.

Securing your life insurance policy with David Pope Insurance Services, LLC will ensure your family is protected and give you the peace of mind you need. We’ll find you a quality life insurance policy at an affordable premium. If your family is looking for a life insurance provider in Missouri, contact us today.