An unendorsed dwelling policy offers limited property coverage. With an endorsed homeowners policy — alternately known as a policy rider — you can raise the limits and expand the scope of your home insurance to protect any value above and beyond your regular coverage. While an unendorsed homeowners policy will cover the value of basic belongings and the house itself from ordinary perils, an endorsed policy will cover any value that you stipulate against all forms of loss.

Learn more about:

Other Homeowner Resources:

Contact Us To Get Your Free Quote

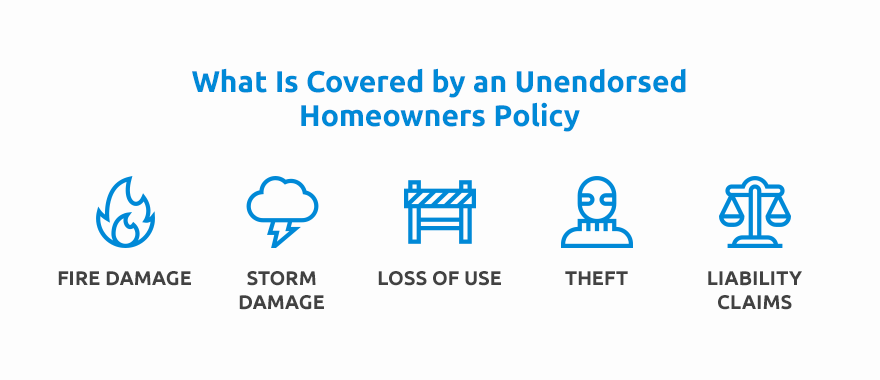

A home insurance policy will generally keep you covered in the event of fire or storm damage. If you and your family are forced to vacate your house in light of a storm, homeowners insurance should also cover your temporary accommodations. A homeowners policy can even protect you from theft and liability.

If your house is damaged in a fire, a basic homeowners insurance policy should cover the costs to repair the house. An unendorsed policy should also cover the cost of damaged or destroyed contents within your home, such as any appliances or furnishings that wind up charred in the blaze. Granted, an unendorsed policy will only cover your belongings up to a certain limit, and the items covered must be recognized as standard household items under the terms of your policy.

Damage incurred by inclement weather is generally covered under an unendorsed policy. For example, if your shingles and siding are damaged in a hail storm, your homeowners’ insurance should cover the costs of roof and wall repairs. Likewise, if strong winds cause a tree or power line to fall onto your house or external structures, homeowners insurance will cover the costs of pickup and repairs.

However, not all acts of nature are covered under a standard homeowners policy. If your neighborhood is swept in a flood, earthquake or tornado, you would need to have a special policy for the peril in question. Unendorsed policies are more designed for the regular perils that often arise in the fall and winter months.

If your house becomes uninhabitable for any length of time, a homeowners insurance policy should cover your temporary displacement costs. If you and your family need to stay at a hotel for a week or two pending repairs to your home, your lodging expenses should be covered under your policy. Homeowners insurance should also cover the cost of meals out and lost income resulting from time off the job due to injury.

If your house is burglarized, a homeowners insurance policy should cover the cost of your stolen items. As long as the limits of your coverage exceed the value lost in the theft, you should be fully reimbursed. However, if you have items of high value that exceed the limits of your coverage, you would need to have a policy rider to account for that extra value in light of a theft.

A homeowners policy should also pay to repair anything damaged by intruders. If a burglar breaks your door or window and ransacks your living room in search of items to steal, homeowners insurance should pay for the new windows and deadbolts.

If a visitor is injured as a guest in your home, your homeowners’ insurance should pay for that person’s medical expenses. A homeowners policy should also reimburse the individual for any loss of income that results from the injury. As long as the limits of your policy are higher than the total hospital expenses and income reimbursement, you should not have to pay anything out of pocket.

An unendorsed home insurance policy will not cover anything of value that exceeds the limits of your coverage. Without any policy riders or special insurance, various perils will also be excluded from your coverage, including the following:

An unendorsed home insurance policy will not cover damage caused by a flood. In Missouri, floods are known to occur, such as the flooding that plagued Branson in 2017. Granted, flood coverage cannot be added to your pre-existing homeowners’ insurance with a simple policy rider, as none cover this particular peril. Due to the widespread damage caused by floods, most insurers exclude this peril because of the high volume of claims and large sums of value that floods place in the balance. To be covered in the event of a flood, you would need to purchase a special flood insurance policy through the National Flood Insurance Program (NFIP).

If you operate a business from home, any equipment exclusive to your business operations will not be covered under an unendorsed homeowners policy if lost or stolen. Anything defined as exclusive to your business would include items that would otherwise not be in your home if not for your home-based business. Items in this category may include copy machines, silk-screen machines and industrial-sized printers. Without a policy rider, a homeowners policy will generally limit coverage to items that are normally owned by homeowners, such as sofas, refrigerators and dinner tables.

Damages caused by earthquakes are not covered under regular, unendorsed homeowners insurance policies. The reason for this exclusion is simple — as with floods, earthquakes can cause excessive damage to hundreds of homes within densely populated suburban communities. If a home insurance company offers earthquake coverage, that insurer could end up processing hundreds of claims on the same day, perhaps from all of the company’s policyholders at once, if a large earthquake were to hit the area.

While Missouri has had several minor, non-damaging tremors in recent years, a massive earthquake on par with the 1811 disaster remains a possibility. However, earthquake coverage is not even offered under any policy rider. To be covered against damage in the event of a quake, you would need to purchase an earthquake insurance policy from a company that specializes in that peril.

A home insurance policy will generally cover the value of your personal belongings up to a certain limit. If your house contains items valued above and beyond the typical household furnishing or fixture, you will need to have a policy rider. For example, if you collect rare antiques or classic, high-priced artwork, your homeowners’ policy will need an endorsement for the category in question. The endorsement will need to be high enough to cover the appraised value against loss from damage or theft. Keep this in mind if you choose to adorn your living room wall with a famous painting purchased at auction for $10,000.

If you have any items in your home that are expected to mature in value, you cannot count on an unendorsed dwelling policy to cover their future value. A homeowners policy will generally cover the value of the basic, everyday belongings inside your home. Furthermore, the coverage limit on a basic policy will account for the value of your property at the time that you sign the policy. Factors such as inflation and maturity of value are not generally taken into account. Without a policy rider, the matured value of a damaged or stolen item will usually be lost, and you will only be compensated for the original value.

An unendorsed homeowners policy will not cover the cost of damages caused by pollution. For homeowners in Missouri, this should be a cause for concern as the state ranks 15th in the nation for polluted air content. The pollution is caused by the noxious gasses emitted from the state’s many mills and factories.

The purpose of homeowners insurance is to protect the value of the personal property against unexpected loss or damage. As such, homeowners insurance is not intended to cover the value of items damaged intentionally by the homeowner. It goes without saying that you cannot file a claim if a member of your household throws an object inside the house and breaks a mirror or shatters a fixture.

If you use your booted foot to reposition your refrigerator and a dent is impressed onto the door, a damages claim will not be honored in that case. If a child throws a rock and shatters a window, this too would be classified as intentional damage, since the parent or legal guardian would be held responsible for the child’s behavior.

When it comes to property, the effects of age can be an unfortunate though not unexpected consequence of time itself. As such, the inevitable wear and tear incurred by your household items will not be covered under your homeowners’ insurance policy, which exists to protect your property again unexpected loss and damage. While you could list your computer on a homeowners’ claim if the tower or monitor get damaged in a fire, you could not file a claim if the hard drive or motherboard fizzle out due to old age.

The same holds true with the house itself. If your roof is damaged in a hurricane, you can file a claim with your homeowners’ insurance company for the cost of roof repairs. However, if your roof gives way because the cedar shingles have exhausted their 30-year life expectancy, you would not have a valid claim because the roof wear would simply be the result of natural causes.

The health of pipes is considered the responsibility of every residential homeowner. When freezing temperatures hit your area, you are supposed to leave your faucets running ever so slightly, day and night, to prevent ice from forming inside the pipes. This step is especially important if you leave your house for several days during the holiday season.

If your pipes freeze, the problem will not be covered under an unendorsed home insurance policy. However, the policy will protect you from damages if the pipes burst. Otherwise, you must monitor your pipes to ensure that they are healthy and capable of performing their functions for the foreseeable future.

As with a basic car insurance policy, unendorsed homeowners insurance will not cover any loss of property value stemming from vandalism. In the event of vandalism to your house, garage or fence, you would generally need to sue the party responsible. If the vandal cannot be traced or otherwise evades accountability, you would have to foot the repair costs yourself. The way around this, of course, is to get a policy rider that protects against vandalism, which could be a wise idea if you live in an area that has been plagued with vandalism and other property crimes.

Contact us to review your policy and provide a free quote.

If the value of your property does not exceed the coverage limit or scope of your homeowners’ insurance, you might not have any need for policy riders. In any of the following examples, an unendorsed policy could easily suffice:

The average residential occupancy lasts approximately 13 years. If you only intend to occupy a house for two years, you might not have enough value invested in the property to merit anything more than a basic, unendorsed home insurance policy.

For example, if you live at your current residence for a vocational job, but plan to move cross-country or overseas in a few years, you might be inclined to keep your furnishings minimal and refrain from collecting anything of value.

Not all homeowners read through the fine print of their home insurance policies, but those who do tend to be mindful of additional coverage options. If you have long known which items and perils do not fall under a homeowners policy, you might have already purchased additional coverage from other insurers to fill those gaps. If you are happy with these policies and feel sufficiently covered against any possible loss, you probably do not have any need for a policy rider.

Some people prefer to live lightly and therefore have little to insure. If you live in a small house with only the most basic furnishings and appliances, you might not have any assets that would exceed the limits or scope of your homeowners’ insurance.

For example, if you live in a basic two-bedroom home and your living room is furnished with a beanbag in lieu of a sofa and a laptop that substitutes for a TV and stereo, any damage caused by one of the named perils in your homeowners insurance would probably never exceed the cost of the items inside your home.

If your town has been free of storms, natural disasters and criminal activity for decades, you might not feel as though your property is in any danger of the perils that fall beyond the scope and coverage of an unendorsed policy. That said, these and other dangers could return at any given time. Just because something has not happened for decades does not mean that it won’t happen tomorrow. Then again, if you feel as though you have nothing to lose, you might need nothing more than standard insurance.

If you prefer to save rather than spend, you might have more value in your bank account than in your home. With car insurance, for example, cars that would cost more to repair than replace are generally not considered worthy of anything more than basic liability insurance. The same principle could be applied to homes. If it would be less expensive and troublesome to move than to have your current house repaired, the property itself might only merit a basic form of coverage.

It would not be wise to content yourself with an unendorsed homeowners policy if you have moved into a valuable home for the long haul. When you consider the various costs associated with maintaining a property and other assets not connected to your home, the consequences of an unendorsed policy could be rather costly. Consider the following possibilities:

If you intend to stay put for the next 10 to 20 years, inflation could make a huge difference in the cost of home repairs during the length of that time. For example, you might move into a home in a newly developing area where properties are inexpensive. As the area develops and becomes more popular, houses such as yours are bound to go up in value.

If you have your house insured for its full value at the time that you move in, you could be seriously uninsured a decade onward as the cost to rebuild that same house catapults due to inflation. With an inflation-guard endorsement, your homeowners’ coverage limit will automatically increase on an annual basis to stay on top of inflation.

Problems with sewage systems generally fall beyond the scope of an unendorsed home insurance policy. Moreover, sewage problems can lead to water contamination and health issues. As such, it can be risky to make do without an endorsement for sewage protection. The cost for a sewer policy rider is relatively low each year, yet the costs associated with sewage backups are generally high.

If your home contains items of value that exceed the limits of an unendorsed policy, you absolutely should get a policy rider to account for this difference. For example, if you have a collection of gold jewelry valued at $100,000, you should never make do with an unendorsed policy that would only allow you to claim one percent of that amount after a theft or fire. You should also get an endorsement if you plan to do business from home, and your operations require the use of non-household equipment.

If you own a river house or a cabin in the woods, you should definitely have the property endorsed under your homeowners’ insurance. An unendorsed policy will not cover these secondary abodes, which nonetheless do need coverage. Just image traveling out to your home away from home, only to find it ravaged by the elements during the months that passed since your last visit. With a policy rider, you could have your hail-ravaged river house restored with no out-of-pocket costs.

For your house, there is homeowners insurance. For your car, there is auto insurance. For your watercraft, there is nothing unless you buy a separate watercraft policy or have an endorsement added to your homeowners’ insurance. With the latter option, your watercraft will be covered against damage or loss. Whether the theft or damage occurs in your driveway or out by the docks, the policy rider will cover the cost of the watercraft.

As a homeowner, insurance coverage is essential for the protection of your home and property, as well as for your own peace of mind. In Missouri, beautiful homes abound, but perils of all sorts can and do arise.

Request a Homeowners Insurance Quote

For more than 15 years, Dave Pope Insurance has secured maximum coverage at reasonable rates for homeowners in the counties of Eureka, Fenton, Gray Summit, Gerald, Grubville, La Barque Creek, Labadie, Leslie, Lonedell, New Haven, Pacific, Robertsville, Saint Albans, Sullivan, Villa Ridge, Washington and Wildwood. With locations in Union and St. Clair, Mo. serving Missouri, Arkansas, Iowa, and Kansas, we can help you secure optimal coverage. Contact us today for a free homeowners policy quote.