When expecting parents prepare for their new baby, they might focus on painting the nursery, picking out a stroller and buying enough diapers. Amid all the exciting plans and arrangements, some parents might forget to change their insurance policies to reflect their new needs. Yet life, home, auto and health insurance are all vital for protecting the health and well-being of a growing family.

Before the big day, ensure you take care of the essential preparations, like becoming financially healthy before your baby arrives. These insurance tips for expecting parents will help you plan for maternity and newborn wellness, so your baby starts their life well-protected.

Jump To:

Life insurance should be at the top of the list of coverage options for first-time parents to consider. Life insurance provides a safety net for situations when the primary wage earner in a family can no longer earn a living. Parents are one of the groups most likely to purchase life insurance coverage because they want to ensure their child is taken care of in case of an accident.

Many parents may think they only need life insurance if they are the primary wage earner. However, any parent with children should consider the effect on their children if they lose the ability to work. According to the Bureau of Labor Statistics, mothers with children under 18 years old contribute to the family income in 71.2% of households. Fathers in the same situation contribute to the household income in 92.3% of families.

The loss of any household income can majorly affect a family’s life.

If you support any dependents with your income or plan to do so soon, you need life insurance. Life insurance provides peace of mind and coverage in the following areas:

Determining how much life insurance you need when you have a baby on the way can be tricky, especially if this is your first child. Keep in mind that if you have a group life insurance plan from your employer, the coverage range might be limited. Depending on your family’s needs, a group plan may not be sufficient. Parents often need to supplement a group plan with an individual life insurance policy.

Here is how to find the best life insurance plan for expecting parents:

With the right planning, expecting parents can find a life insurance policy that provides the coverage they need at the price they can afford.

Determining how much life insurance you need when you have a baby on the way can be tricky, especially if this is your first child. Keep in mind that if you have a group life insurance plan from your employer, the coverage range might be limited. Depending on your family’s needs, a group plan may not be sufficient. Parents often need to supplement a group plan with an individual life insurance policy.

Here is how to find the best life insurance plan for expecting parents:

With the right planning, expecting parents can find a life insurance policy that provides the coverage they need at the price they can afford.

Home insurance isn’t likely to change just because your family gains a new addition. However, when you add a new member to your family, you may feel you need more space to grow. Many parents choose to move because they need an extra bedroom for the baby or want to live closer to a specific school system.

Relocating to a new house or building a new addition to your current one could increase your home insurance payments. You might consider changing your home insurance policy altogether if you’re in the following situations:

Buying a new house in preparation for a baby is common for first-time parents. A small studio apartment in the middle of the city might not be your ideal starter home for raising your child. Many parents want a house with room for playing outside. Quieter neighborhoods are also appealing, as are homes closer to family-friendly amenities like parks and day care.

However, moving into another house is one way your home insurance costs can increase significantly. You might find that your insurance plan for a smaller home or an apartment no longer covers your needs. In addition, upgrading to a home with higher square footage usually increases monthly mortgage payments.

If you are interested in buying your first home in preparation for a new baby, you will need to get homeowners insurance. Homeowners insurance is more expensive than renters’ insurance, so if you upgrade to a larger home, you should budget for the extra expense.

Another way that parents’ home insurance could change is if they make major home improvements to their current house. Safety upgrades like mold remediation, refinishing floors and painting or staining should usually be completed before a baby’s arrival. You might also want to complete a more extensive home project, like adding a bedroom or bathroom to your house.

Whatever kinds of upgrades you make, you’ll need to let your insurance company know so they can adjust your coverage. Underinsuring your renovated home can leave you at risk if an accident occurs.

Improving your living space can significantly affect home insurance. Parents should consider taking the following steps to prepare for a change in homeowners insurance:

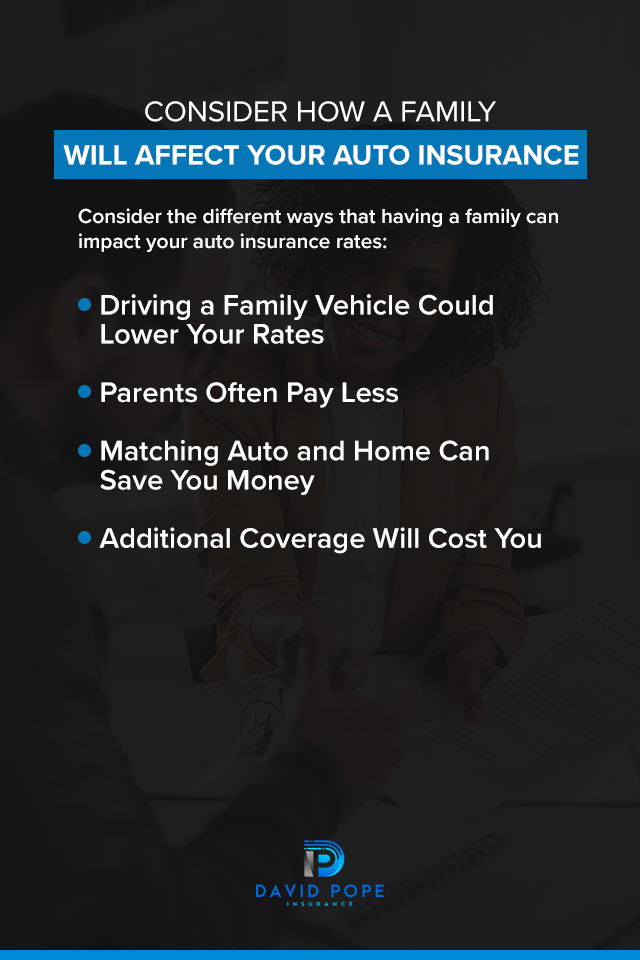

Having a new baby could also affect your auto insurance costs. As with home insurance, having a child only affects auto insurance indirectly. Consider the different ways that having a family can impact your auto insurance rates:

Many parents find the need to drive a larger car or sensible minivan when they welcome their first child. Your car needs to accommodate a bulky car seat along with all baby gear like a stroller and a diaper bag. Larger vehicles are also typically safer in the event of a crash, making them a good choice for parents.

Switching to what insurance companies call a family vehicle could positively impact your rates. Sports and luxury vehicles are more costly to insure because they have more expensive parts and their drivers tend to be less careful. However, drivers of minivans often have babies on board. These cars tend to be among the cheapest to insure because drivers are often more cautious, so insurers trust they will make fewer insurance claims.

Many insurance companies charge parents lower auto insurance rates than single people and even married couples without children. This is because parents tend to be responsible drivers, knowing that it’s up to them to get their family home safely. They will probably end up filing fewer claims, making them cheaper for an insurance company to insure.

New parents are always on the hunt for ways to save money. Every penny saved is more they can put toward new diapers or other funds for their bundle of joy. Parents who are also homeowners could qualify for savings on their auto insurance when they bundle it with a home insurance policy from the same insurance company.

Increasing your coverage can give you peace of mind and help you protect your little one wherever you travel.

Additional coverage can protect you, your family and your finances in adverse situations. New parents might be interested in adding personal injury protection insurance to their auto policy. In case of an accident where you or your passengers are injured, this no-fault policy will help pay for your medical bills and ongoing care.

Another kind of coverage extension that could be appealing to parents is a roadside assistance plan. Roadside assistance can come to the rescue if you run out of gas, lock yourself out of your car or need a tire changed. Even if you know how to perform minor repairs on your vehicle, adding a crying baby to the mix can cause additional stress. This addition to your policy can help you navigate those unanticipated situations.

With so many coverage options out there, it is essential to shop around and compare prices for auto insurance. Going straight for the minivans at the car dealership may not get you the cheapest rates. It’s still important to compare the cost of insuring each car you’re interested in before you make a purchase.

In addition, carefully analyze multiple bundle options to determine if they save you money. If you find two policies that cost less than a bundled policy, your best bet is to buy them separately. Discuss your options with your insurance agent to determine whether bundling can help you lower your costs.

Young, healthy people may not feel like health insurance is necessary for them. According to the 2019 American Community Survey, Americans between the ages of 19 and 34 are the least insured age group. This age range is when most people in the U.S. become first-time parents, which makes it a necessary time to purchase health insurance coverage.

Having insurance during pregnancy is vital. Adequate health coverage can help pay for routine checkups and screening tests that keep mom and baby healthy. Childbirth and maternity care are considered essential health services under the Affordable Care Act (ACA). This policy ensures that most health insurance policies cover a policy holder’s pregnancy and childbirth.

The best insurance plans for pregnancy are the ones that give mother and baby plenty of coverage before and after delivery. Besides providing essential coverage for new moms, adding health insurance can benefit a new family in several ways:

Finding the best health insurance during pregnancy should be uncomplicated. Planning may take time, but in the end, it will be worth it to have all the information you need to make the best decision for your future child. Remember the following suggestions when shopping for health care coverage for your new baby:

One of the best ways to prepare for adding a new baby to your health insurance is to obtain a list of the exact services your health plan offers well before your due date. It can also be helpful to determine what your out-of-pocket expenses will be, so you can plan for those costs ahead of time.

Expecting parents have many insurance decisions to make before their bundle of joy arrives. Each family’s coverage needs are unique. Speak with a local expert who understands the health, life, auto and home insurance options available in your area so you can find and understand the plan that works best for you.

David Pope Insurance is a local insurance provider with over 20 years of experience providing a range of insurance services. Our expert team can help new parents reach financial stability by finding the lowest rates for the coverage they need. We offer fast and flexible quotes designed to work for you.

Contact us today to request a quote and learn about how David Pope Insurance can benefit you.