Perhaps you want to retire after long years of working in the insurance industry. Or you’re ready to leave the industry but want to ensure the business is in good hands. If so, you may be thinking about the various steps to selling an insurance agency and the pros and cons of selling a book of business versus selling the company itself. While selling the company may seem more straightforward, handing off the book of business can be a more profitable route.

A book of business is a list of clients and services. The individual or company that provides the services keeps the book updated. Some professionals that may use a book of business include financial advisors, insurance providers, lawyers and investment bankers, among other people.

A business or individual uses a book of business to track their clients and the services they provide for those clients. A book of business should include a comprehensive list of clients you’ve worked with, not just current clients. Remember to add information about new clients and update the list as needed. A good book of business will also include details about customer transactions, client demographics, current assets, your total calculated revenue and any referrals made.

One of the most important ways you can update your book of business is by developing good relationships with clients through network events and social media platforms. Maintaining those relationships can help ensure you have a continued customer base for years to come.

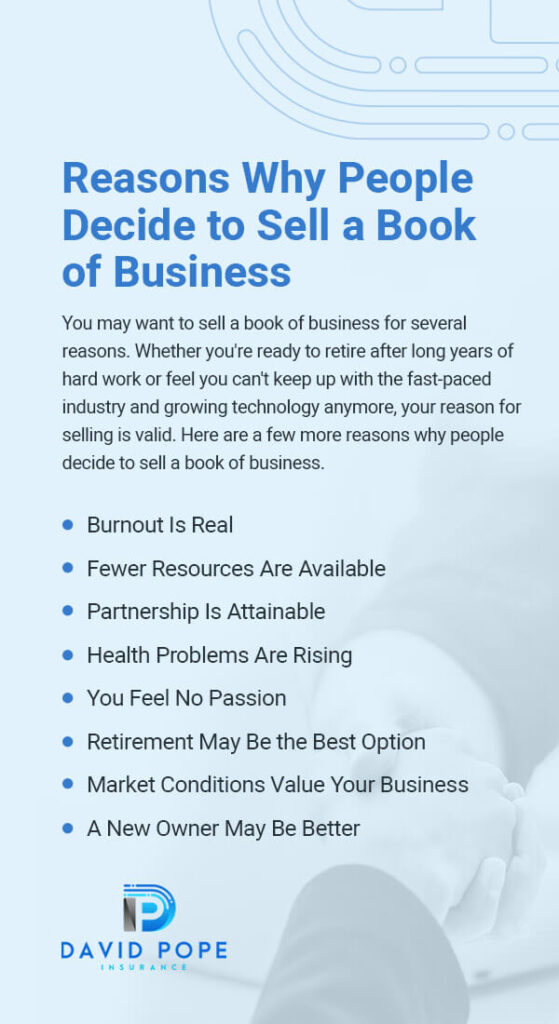

You may want to sell a book of business for several reasons. Whether you’re ready to retire after long years of hard work or feel you can’t keep up with the fast-paced industry and growing technology anymore, your reason for selling is valid. Here are a few more reasons why people decide to sell a book of business.

After years of dedicating your time and energy to the business, it can be draining to continue working for the company. Keeping up with the finances and the growing clientele may be more stressful than you can handle. If you feel you are experiencing burnout, it may be a good idea to sell your book of business and let someone else take over the more challenging tasks.

After accomplishing so much in the insurance sphere, you may have eventually run out of resources for your business. It may be your best option to sell your book of business to a larger company with the resources, technology and management skills to take over for you. You might not have any more financial capital that you can use to invest, and a larger company can pitch in its resources that allow your career to grow and thrive.

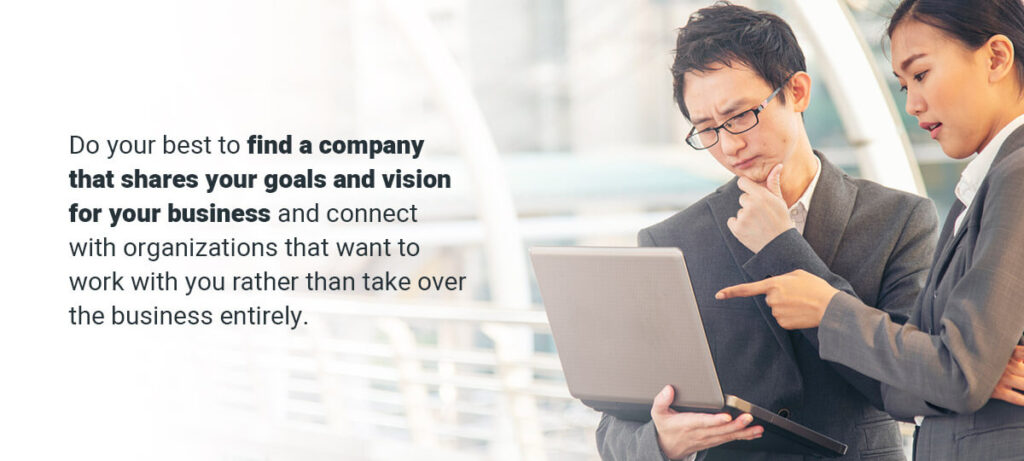

Sometimes you may be looking to sell your book of business while also building a partnership with another company. Do your best to find a company that shares your goals and vision for your business and connect with organizations that want to work with you rather than take over the business entirely.

The longer you work for the business, the more you may deal with health problems as you age. If you are starting to see your physical or mental health decline over time, it may be time to consider selling your book of business. While it may be best for you to have someone else take over the finances or overall operations, you can be involved as much as you want. However, if the stress of working has become too much for you, it’s best to prioritize your health.

If you no longer feel the same passion or fire for the business as you used to, consider selling your business to someone who may still be interested in the industry. Perhaps your passion has lessened because you’ve found a new career or ambition to explore. Whatever the case, finding a new owner with a drive for the business will ensure it continues to run smoothly without you.

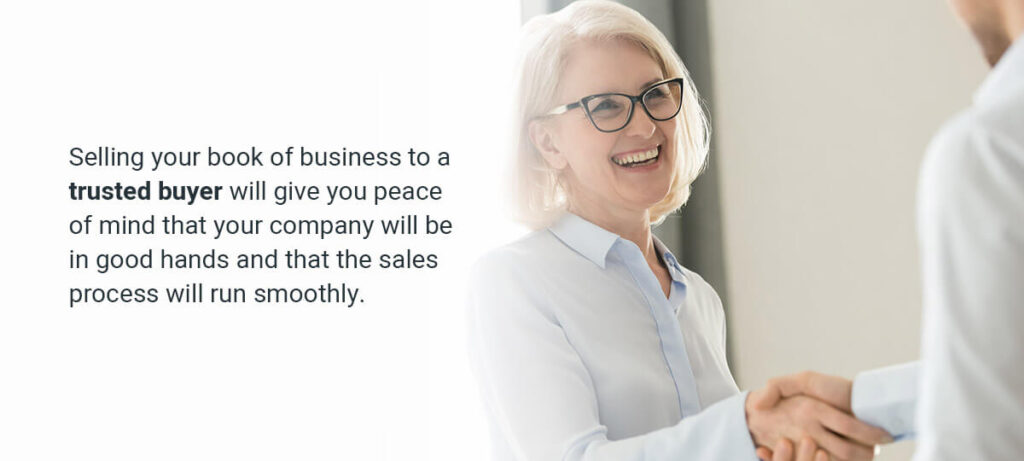

If you’re at the age where you want to consider retirement, you’ve likely worked very hard at your business and seen lots of rewards. Now it’s time to step back and enjoy some time for yourself. Selling your book of business to a trusted buyer will give you peace of mind that your company will be in good hands and that the sales process will run smoothly.

Your company’s value may fluctuate depending on the market’s current conditions. While you may be thinking about selling your book of business, consider the market before making any concrete decisions. Examine areas like interest rates, buyer demand and the profitability of local agencies. All these factors may change your agency’s value, and you’ll want favorable market conditions to sell your agency at a fair price.

Selling an insurance book of business to a new owner may be a good option if you think a peer or employee could bring new ideas to the table. Sometimes loyal employees or well-trained family members are ready to take over the company. Allowing someone else to step up and lead may be a good decision, especially if you are experiencing burnout or are ready to retire.

Contact Us TodayGive Us a Call

Selling an insurance book of business rather than your entire agency has many benefits. For one, it may be challenging to sell the whole company if it’s losing money or isn’t as profitable as it once was. Most companies are unwilling to buy a failing business. However, selling your book of business can satisfy both parties.

Another benefit to selling your book is that you may still be able to have input at the company and continue selling insurance. Depending on your non-compete terms set during the sale, you may be able to pursue other areas of insurance while still retaining all the marketing tools, employees, buildings and office supplies you need to keep the show going.

Selling your book of business may also lead to liquidating your agency. Liquidation means selling your supplies and buildings, which may be more profitable in the long run. However, your business may be worth more as an entire agency rather than in pieces. Considering both options and the underlying pros and cons of both decisions is essential.

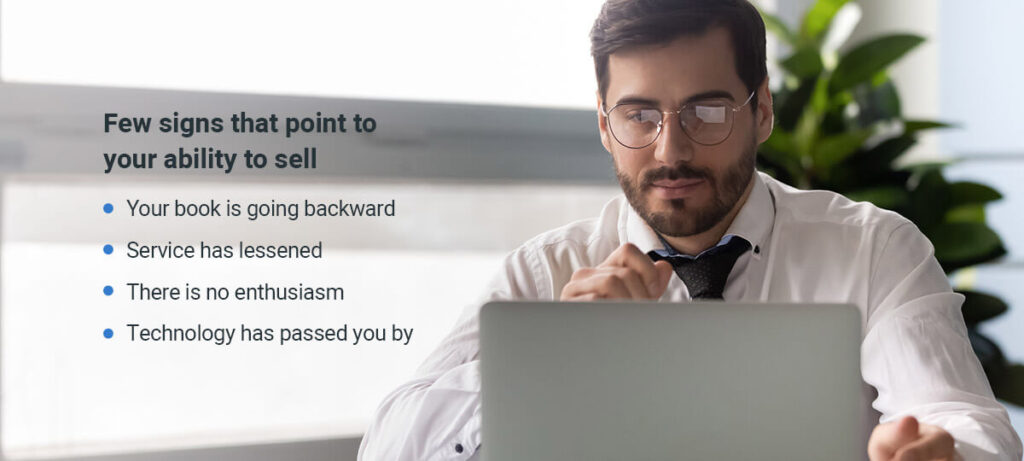

So, you’ve decided that selling your book of business might be the best option for you, and you’ve weighed all the benefits. But, how do you know if you’re ready? Here are a few signs that point to your ability to sell:

Determining how much your insurance book of business is worth is the most crucial step in the selling process. After deciding to sell, you’ll want to get the best price for your agency by calculating your total earnings and negotiating a selling price. Explore the various ways you can profit from your sale.

The value of your business is often based on your annual gross commission and your adjusted Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA). The annual gross commission is the amount of money your agency makes per year. Calculating your EBITDA can also help when it comes time for wise investments. To calculate your EBITDA, add all the company’s profits and assets and subtract any loans or expenses over the years. Adjust this total for employee salaries, rent or the cost of hiring a replacement. Remember that your EBITDA should also be evaluated along with your net income and other capital costs to determine an accurate number.

Calculating your total earnings can tell you which assets and products are worth a fair amount of money when you sell. If your business has grown its investments over the years, it will be worth more money in the long run. After gathering your assets and products and subtracting any debts or loans, you’ll have a good idea of your total earnings.

When it comes time to sell, you can provide an accurate assessment of your business to the buyer. Remember that many companies sell for over four or five times the EBITDA, but your earnings won’t be the only factor buyers consider. Buyers will also look at your policies and premiums, client reports and reviews and large clients’ opinions to determine your company’s strength and value.

Any buyer considering taking over your agency will evaluate the risks of buying the business. Many sales can be risky depending on whether or not your agency has lost money over time or is struggling financially. Buyers don’t want to lose money and want to be reassured that their investment will be worth it.

Here are a few high-risk signs that buyers will consider:

A smart buyer understands that there are always some risks associated with a sale. However, you still want to present your company in the best possible light to ensure any potential buyers will be more likely to remain interested in the agency and willing to take over.

A solid financial plan will ensure you receive the money you deserve from selling an insurance book of business. Encourage potential buyers to utilize third-party financing, which shows the buyer is confident they will receive enough money in loans to buy the company while out-bidding other parties. Third-party financing can help you sell your agency for its full value, and the buyer won’t need to find complex lines of credit to acquire the company.

Here are a few more benefits of using third-party financing:

A solid financial plan will help both parties reach a beneficial agreement. As financial responsibility passes from you to the new owner, you’ll want to ensure they are left in a good spot after you finalize the sale.

After you’ve agreed to the terms and the sale is completed, you can decide how you would like to be paid. There are typically three different methods of payment that you can consider. Keep in mind that each one comes with its own pros and cons to consider. These methods are lump sum, over time and earn-out payments.

The lump sum method is one of the most straightforward forms of payment that you can receive. This method often requires the buyer to take out a loan to compensate for the total price. Afterward, they write you a check for the full amount, paying you the entire purchase price at once. The lump sum method is one of the fastest ways to receive a payment.

However, the lump sum method is often risky for the buyer, and they may not agree to it at first. For example, they may worry that after they acquire the business, the projected growth or sales will be less than predicted. Buyers don’t want to spend their money without any return on investment, so they may make a low offer.

The main advantage of this method is that you receive the money all at once.

The over time method is also a straightforward payment process. One of the benefits of this method is that it removes some stress and pressure from the buyer. They won’t be required to secure a loan upfront and can instead pay an agreed-upon percentage of the sale upfront. The buyer may then give you a note for the rest of the payment, or you can receive gradual payments in a specific amount over time.

This method poses some risks for the seller. The buyer may try to downsell you to save them money in the long run, so it is essential to find a buyer you trust. However, a few advantages may come with this payment process. Getting paid over time guarantees you will receive the money, and you can always sell the note to a note-purchasing company. Discussing this prospect with the buyer may drive them to offer a higher value for your business than before.

While the earn-out method can be riskier for you as the seller, it may also come with high rewards and payments. This method has the buyer paying you around 60% to 80% of your company’s value upfront and the remaining percentage to you over time. As the agency grows and prospers under new management, your payments will likely increase.

If there are discrepancies between the seller’s and the buyer’s valuations, the earn-out method can be a great way to resolve these differences. The buyer can absolve themself of financial responsibility if the business doesn’t grow as projected after the sale. At the same time, if the business does well, you’ve ensured that the sale price depends on your company’s profitability. Remember that the earn-out method works best if both the buyer and seller work out their top priorities.

Relieving the risk for the buyer is perhaps the best part of this method. Your insurance book of business may often be valued highly, especially if there is reassurance that the company will be profitable for the new owner. Always ensure you can trust the new buyer before agreeing to this particular payment method, but remember that this process may make you the most money in the long run.

David Pope Insurance Services, LLC has been a trusted home, auto, life and commercial insurance provider since 2005. Our company has years of experience writing policies and is a reliable provider of umbrella insurance coverage quotes. We are dedicated to giving our clients the best insurance policies and bundles at the lowest possible rates. David Pope Insurance serves the states of Arkansas, Colorado, Illinois, Iowa, Kansas, Missouri, Nebraska and Tennessee and offers modern techniques to bring you fast solutions and reliable customer service.

Selling your book of business to David Pope Insurance ensures your company partners with a reliable agency that has been in the industry for almost two decades. Our experienced team will work with you and your business to find the best valuation for your agency. If you feel it is time to sell your book of business, consider David Pope Insurance. Contact us today to speak to a representative or call us at 636-583-0800.