Insurance companies can help you manage unexpected harm to your property. Finding the right insurance helps protect you and relieve the financial strain that sudden damage can cause. About 1 out of 20 homeowners file an insurance claim yearly, so it’s always good to be prepared for filing a claim.

Keep in mind that reimbursement requires more than simply filing a document. You’ll have to gather records of your car or home and understand the limitations or exclusions of your current insurance policy. Stay in touch with your provider throughout the process to ensure you receive the necessary reimbursements after a claim.

Speak with our experienced agents for honest advice and support before you take the next step.

Get Expert Insurance HelpAn insurance claim acts as a formal request for money. Often, insurance helps you pay for any repairs or expenses due to unexpected damage to your property. Some policy events covered by your insurance may include a car accident or robbery.

The Insurance Information Institute states that car insurance claims increase yearly. Meanwhile, the process may look a little different depending on the insurance claim you file. When filing an auto insurance claim, an adjuster will likely want to investigate the circumstances that led to the damage. If your claim is approved, you should receive a check for your insurance money.

On the other hand, homeowners insurance policies offer financial protection if your property is struck by an accident, extreme weather or unexpected damage. If you have a mortgage on your home, many banks or lenders will require that you buy insurance beforehand. Even if you own your home, buying insurance may still be a good idea to prevent hefty expenses should the worst happen. Making an insurance claim may help you manage your losses and expenses during an emergency.

There are many situations where it may or may not be appropriate to file an insurance claim. Consider your situation carefully before filing the paperwork, as some insurance companies may reject your claim based on the circumstances of the accident. Here are a few reasons to file an insurance claim:

Contact Us for More Information

While there are many situations where it is appropriate to file an insurance claim, you should also understand conditions where you shouldn’t file one. Here are a few cases where it would be best to avoid an insurance claim:

Consider some essential factors before filing a home or auto claim. You’ll want to be completely prepared for every scenario should you experience an accident or emergency that calls for compensation. Here are 10 things to consider before you submit insurance claims.

It’s best not to wait to file a claim. Filing quickly can help you get the funds you need to make repairs sooner if you’re approved. Knowing before an emergency happens that you’d need to gather documents and other forms of proof can help you prioritize organizing information for your claim.

Showing that you understand how to move your claim through each step is a good sign for insurance companies. Understand what your policy covers and how you can best follow the claims process in your policy. While some areas of the policy may be open to interpretation, it is good practice to develop a robust strategy should you need to file a claim.

While filing an insurance claim can be complicated, you can familiarize yourself with the predictable parts of the claims procedures. Many insurance companies expect you to understand what has been damaged and how much you wish to be compensated. Be diligent in preventing more damage while allowing the insurance company to investigate the situation. This may look like thoroughly documenting the damaged property or developing a proof of loss statement.

An expert can help advocate for your situation. Try consulting with a public insurance adjuster who may be able to find the best outcome for your needs.

Make lists of anything you think would be necessary to the insurance claim. This includes items that need replacing, their prices, the date purchased and any relevant receipts related to what you’ve lost.

One of the best ways to prepare for the process is to learn how to work with insurance adjusters. While you don’t want to admit guilt to any wrongdoing, it is also best to be truthful as much as possible to both the adjuster and the insurance company. If they find out you’ve misrepresented or concealed information, you could be liable for insurance fraud.

Another great way to work with adjusters is to document your interactions as much as possible. A journal or spreadsheet can help you organize dates and times of conversations. You may also include a small paragraph about details of your communications, copies of reports and statements.

Some choose to hire their insurance adjuster — public employees may help you avoid hidden risks or issues you haven’t seen before. However, remember that they may also take a percentage of your insurance claim should the claim be accepted.

Try to report and document damages as much as possible before and after the insurance claim has been filed. The reporting and documenting process may require a few specific steps, including:

Some policies may require that you make some repairs to your property once you’ve thoroughly documented the damage. This ensures your property is protected from further damage in the future. Failing to make reasonable repairs could result in insurance companies denying your claim due to personal negligence.

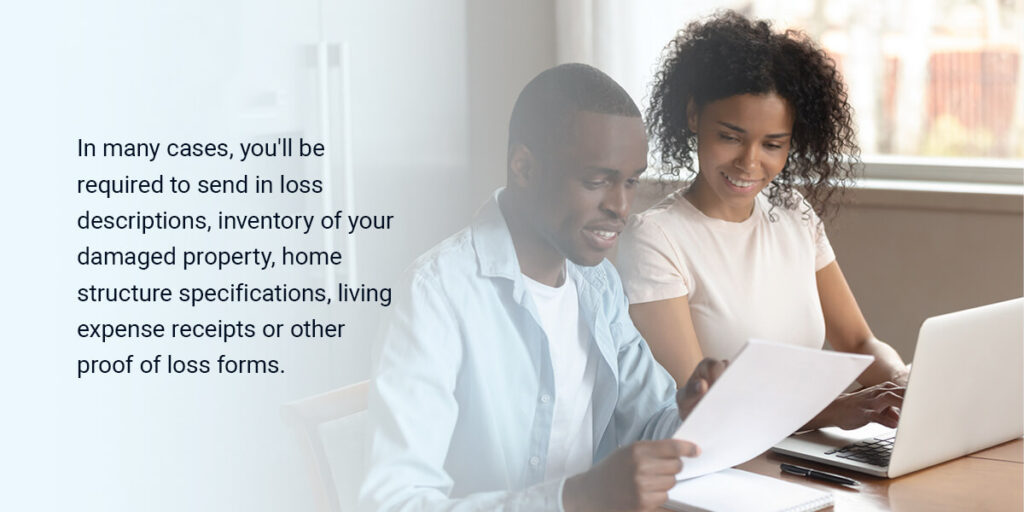

While an adjuster often lets you know when and how to meet your deadlines, it is still good practice to ensure you stay on top of paperwork. In many cases, you’ll be required to send in loss descriptions, inventory of your damaged property, home structure specifications, living expense receipts or other proof of loss forms.

Failing to fill out paperwork on time could result in a denied claim. Read your policy thoroughly and contact a professional if you’re still unsure about your coverage.

Understanding your policy is crucial before filing any claim. Let us help you review your coverage and avoid costly mistakes.

Schedule a Coverage ReviewClaiming home insurance may be a tricky process. Likewise, the auto insurance claims process has its essential steps. You’ll want to familiarize yourself with the mistakes others have made to avoid them. Some common insurance claim mistakes include:

Now that you’ve gathered some car and homeowners insurance claim tips, it’s time to understand the steps for filing the insurance claim. There are a few things to know when claiming car insurance or considering a home insurance policy. Here are the steps to filing an insurance claim.

The first step to filing a claim is to call the police as soon as the incident occurs. Whether you experienced a robbery or a car accident, the police can assess if someone was hurt or if your property sustained significant damage. The police will also fill out a report that explains what happened in detail, and this report may make it easier for insurance companies to process your claim.

Aside from collecting the police report, make sure you gather the names of all police officers and emergency personnel who responded to your call. Write down details of the event from your perspective and save this information for later.

Next, you’ll want to assess what damage you can see and gather information from all parties involved.

If you’ve been involved in a car accident, gather information like the name and phone number of other drivers, insurance policies, license plates and car information and any notes from conversations with the drivers or passengers. You’ll also want to take photos of the accident and the surrounding area to provide proof and context to your insurance company later. If you’ve been injured, keep a copy of any doctor reports, bills or documentation to ensure you’re compensated.

For those filing homeowners insurance claims, be sure to take detailed photos of the damage. If you’ve been robbed, make a list of any items that have been taken, their price and other relevant information related to your property. Make a note of any damaged items and take videos or gather receipts should they be needed later.

Contact your insurance agent and inform them of the accident or damage to your property. Now is a great time to ask your agent some burning questions, like how long auto insurance claims take or when to expect the homeowners claims process to end. Try to gather information on who to report to, how long you’ll have to file the claim and what information you’ll need to file the claim.

Finally, you’re ready to file your claim. Many companies allow you to do so online or through an app on your phone. You can also call your agent or file a claim through email or fax. Once you’ve filled out the form or called your insurance company, try to stay on top of the claim and resolve it as soon as possible. Stay aware of any important deadlines or forms that the company requires.

After filing the insurance claim, your insurance company will likely send an adjuster to assess the damage or investigate the accident. The adjuster will look over every fact of the theft, accident or incident to determine what caused the car accident or home damage while using this information to tell the insurance company what they should pay. If you are working with another company’s insurance adjuster, ensure you provide thorough documentation and honestly communicate your injuries.

From paperwork to documentation, our team is here to guide you through every step and maximize your benefits.

Talk to a Claims Specialist TodayDavid Pope Insurance can help walk you through the process for claiming car insurance or give you tips for filing a homeowners insurance claim. Our company’s services help you find the right insurance to fit your needs, whether you’re looking for a home, auto, life or commercial insurance coverage. Contact us today to learn more about our services or request a quote online to begin your insurance journey with David Pope Insurance.