Life insurance is one of those topics that is sure to cause an emotional reaction. After all, investing in life insurance is acknowledging the sober reality that death is an inevitable part of life, and sometimes, it comes all too soon. When such a tragedy occurs, for some, it could leave their family in a difficult financial position. While it’s healthy to adopt an attitude that does not expect the worst, it is also wise to be prepared for the worst-case scenario. Being ready for the what-ifs can keep you from worrying about them.

If you’re interested in learning about life insurance and whether it’s something you should consider, this guide is for you. We’ll discuss when life insurance is and is not worth it, what the end value is, what types of policies to consider and what can qualify and disqualify you for life insurance.

As we discuss life insurance, it’s important to remember that life insurance is fundamentally a different sort of product than other types of insurance. When most people think of insurance, they likely have an idea of insurance as something that can help to pay for damages or a mishap that occurs — big or small — so that it doesn’t cause a sudden financial strain.

Jump Ahead to:

Auto insurance may help to pay for minor damage like a cracked window or major damage affecting your whole car. Health insurance can help pay for everything from routine check-ups to more major medical procedures, such as a surgery. With life insurance, there is only one event the insurance covers, and it can only happen once: the death of the policyholder. A death isn’t something that can be “covered” or “paid for” in the traditional sense. In this way, life insurance differs dramatically from other types of insurance.

However, as with other types of insurance, life insurance is a way of preventing a sudden financial strain that could fall to the deceased’s dependants. If you have people who depend on you to help make ends meet, life insurance can be an invaluable safety net that protects your family from financial hardship and gives you peace of mind while you’re enjoying life with your loved ones.

Life insurance isn’t for everyone, but for some people, it’s definitely worth it. How do you know if life insurance is worth it for you? To make that determination, think about who would be affected financially by your death. Do you have a spouse, children or other family members who depend on your income for their financial stability? If so, then life insurance is a wise move. Also, think through the expenses that might fall to your family if you were to die. Would they be able to afford them? If not, then life insurance would be a responsible way of providing for that need in advance.

These questions are a good place to start, but we can get more specific. Let’s look at a list of situations where having a life insurance policy in place has major potential benefits. If you identify with any of these scenarios, then you should strongly consider purchasing a life insurance policy:

If you have a spouse who relies on your income for their financial security, then they will feel the financial effects of your absence right away. A death benefit will give them time to grieve and eventually find a job without experiencing financial hardship. In some cases, depending on the sum your death benefit provides, they may not have to go to work for a long time, if ever.

If you have, or plan to have, children who will be financially dependent on you, then you should plan for them to be provided for if you no longer can. A 2016 survey revealed that 20 percent of households with children who are minors do not have life insurance. Of these uninsured families, 62 percent recognize that, if the primary wage earner died, they would experience immediate financial trouble.

If you care for an elderly parent or relative who would need professional care if you were no longer there, then having life insurance and listing them as a beneficiary can help to cover the necessary costs to maintain their quality of life — whether it goes toward a full-time caregiver or a nursing home.

Whether you have partial ownership in a business or you own your own business and employees depend on you for their income, having life insurance provides a buffer to keep you from leaving those who depend on your financial contributions in a lurch in the event of your death.

If you have significant debts, which for most people includes a mortgage, then these debts could become a burden for your heirs if you die. If you have life insurance, then the death benefit your beneficiary receives can be used to go toward your loans or even pay them in full, lifting the burden from them.

Even if no one depends on you financially, you have your final costs to consider. According to the National Funeral Directors Association, in 2016, the average cost of a viewing, funeral and burial that included a vault was $8,508. Add onto that the cost of a marker or headstone, which can be very expensive, and your family may experience some financial strain unless they have a death benefit to cover these expenses.

While there are many people whose financial situation makes life insurance a wise choice, for others, life insurance may not be necessary. As of 2018, 40 percent of Americans are not covered by life insurance. While it’s safe to say that some of these people really do need life insurance and may even realize their need, some may be justified in their decision not to have it.

Here are some reasons why you may not need life insurance:

If you don’t have a spouse or children who rely on your income, then, while your death would certainly leave loved ones in a state of grief, you wouldn’t leave anyone in a state of financial hardship. One reason why a single person may still want life insurance is to cover their funeral and burial expenses.

Since life insurance is primarily designed to protect against an untimely death, if you are of advanced age and have already retired, then traditional life insurance policies aren’t always the smartest investment. However, you may want to consider an annuity, which we will discuss.

Some people may choose to have life insurance coverage when they have children who depend on them financially, but if your children have grown up and are now self-sufficient adults, then you don’t need to leave them a death benefit. Of course, if you have a spouse who is your dependent, you still need to consider their financial well-being.

In most cases, if you have dependents, whether it be a spouse or children, you’ll want life insurance to make sure they’re well cared for. However, if you have built up enough wealth and income streams to keep your family comfortable, then you can count on these and don’t also need life insurance.

Like all types of insurance, there is a cost associated with life insurance. For many families, the premiums they pay come out of a tight budget. Considering the financial cost, you have to be convinced life insurance is worth it. So, what’s to be gained by having life insurance? In other words, what is the end value?

Life insurance policyholders hope that they will never reap the benefits of life insurance, but in the event of a death, the policyholder’s beneficiaries will experience some important benefits. Here are various aspects of the end value to a person’s family that may motivate an investment in life insurance:

Ultimately, the end value of life insurance to you, the policyholder, is that you can rest easy knowing that your loved ones won’t have to suffer financially if you die. Investing in life insurance is one of the most responsible things you can do for your family if you have dependents. You can hope you’ll never need it, but you can rest easy knowing it’s there if you ever do.

If you’re considering purchasing life insurance for yourself or a loved one, the next step is to understand the different types of policies that are available. As with all types of insurance, one size does not fit all. Policies differ based on premium rates and how much financial coverage you gain.

However, if you’re used to the way other types of insurance policies work, as mentioned above, be aware that life insurance policies have some important differences from other types of insurance. Consider auto insurance, for instance. You can choose a level of coverage depending on how much you’re willing to pay and, in turn, know what sorts of mishaps your insurance will cover financially. In the case of life insurance, there aren’t different potential mishaps it protects against, so you don’t choose a policy based on which costs you want to be covered.

The main differences from policy to policy are how much you pay in premiums and potential fees, how much the life insurance company pays out in the event of a death and how this sum is distributed to the beneficiary. Let’s look at four types of life insurance policies to consider: universal, whole, term and annuities. For each type, we’ll discuss what sets it apart from the other policies and what pros and cons to think through. Of course, not all life insurance companies offer the exact same policy options, and policies can sometimes be customized, so be sure to pay attention to the exact terms of a policy if you’re considering investing in it.

Whole life insurance is a type of permanent life insurance, meaning, as long as premiums are paid, it will last for a person’s lifetime rather than running out at a certain point. Whole life insurance is the most common type of permanent insurance policy. The main thing that sets it apart from universal insurance, another type of permanent policy we’ll discuss, is that whole life insurance offers greater stability but less flexibility.

Like other types of permanent life insurance policies, whole life insurance includes an investment savings component. Often referred to as the cash value, this component functions much like a savings account. Because whole life insurance combines life insurance with investment savings, premiums consist of two different components: the cost of insurance, which goes toward the death benefit, and savings. With whole life insurance, your premiums are guaranteed to remain constant. So, no matter how the cost of living increases, your premiums will remain the same month-to-month or year-to-year.

The part of your premium that goes to savings is added to your policy’s excess cash value. This value not only increases due to these payments — it can also grow, tax-deferred, over time based on interest determined by a formula the insurance company decides. Typically, with whole life insurance, this accrued interest is adjusted annually. With whole life insurance, the interest rate is guaranteed by your insurance company. You may receive additional cash growth from dividends as well.

There are two main benefits of having a savings component with your life insurance:

When the insured person dies, beneficiaries will receive the insurance company’s death benefit, but any remaining cash value that was accrued will stay with the insurance company. If there are any outstanding loans, their cost will come out of the death benefit, and unpaid interest will come from the remaining cash value.

Here is an overview of the pros and cons of whole life insurance as a policy type:

Pros

Cons

Universal life insurance, also sometimes called adjustable insurance, is another form of permanent coverage, meaning, as long as your premiums are paid, you will remain covered for the duration of your life. Like whole insurance, it combines life insurance with investment savings and delivers the same benefits, including the potential for self-sustainability and access to savings. What makes universal life insurance unique compared to other types of permanent insurance policies is that universal life insurance is more flexible and fluid.

The flexibility comes from the fact that the policyholder has some say in setting their life insurance rates and death benefit, as well as how much of their premium will go toward the policy’s death benefit and how much will go toward the policy’s cash value. To put it simply, this means universal life insurance can adjust to your financial abilities at any given time.

The other main difference compared to whole life insurance is that the interest rates for your cash value are not guaranteed. Instead, they fluctuate depending on the current market. Your interest will most likely update monthly rather than annually, as it tends to do with whole life. The growth pattern your cash value experiences can differ based on whether your universal life insurance policy is variable, indexed or current assumption. Your cash value growth will also be affected by the premium amount you pay and whether you tap into your cash savings.

Because of these many variables, and especially due to the inconsistencies of market interest rates, there is some risk associated with universal life insurance. Some insurance companies may offer a guaranteed minimum interest rate which would apply if the market rate dips below this minimum. A guaranteed rate mitigates much of the risk.

Here are the main pros and cons to think through if you’re considering a universal life insurance policy:

Pros

Cons

Term life insurance policies are the simplest to understand. For this reason, many people think of term life insurance as “pure” insurance. The simplicity of term life insurance is part of what makes it a popular option. Term life insurance, and specifically, 20-year term policies, are the most popular life insurance policy type. With a term life insurance policy, you pay regular premiums and, in return, you know that your beneficiaries will receive a death benefit if you die while the policy is active, and premiums are paid.

Term life insurance is a good option for people who expect to have enough assets built up in the future to render life insurance unnecessary but who need coverage right now. In other words, their dependents would experience financial hardship if the policyholder were to die in the coming year or some period of years. To ensure their beneficiaries’ financial security, they want to know they will pass on a death benefit from their life insurance.

In addition to being simple and straightforward, term life insurance is also more affordable, at least in the short-term. The premium you pay throughout the term typically remains constant and is based on your age and health conditions when you begin the policy. However, some long-term policies may involve increasing premium rates. Make sure you understand whether your premium is guaranteed to remain the same or whether it may increase over the duration of the term.

Because term life insurance doesn’t include extra features, it doesn’t carry any extra fees or maintenance costs, which also contributes to its affordability. Of course, you forego the benefit of the investment savings component, but some people prefer to keep their savings separate from their life insurance and stick to a traditional savings account or another investment option. Even if you keep savings separate, you could still use the money you save to help pay for your term insurance premiums down the road.

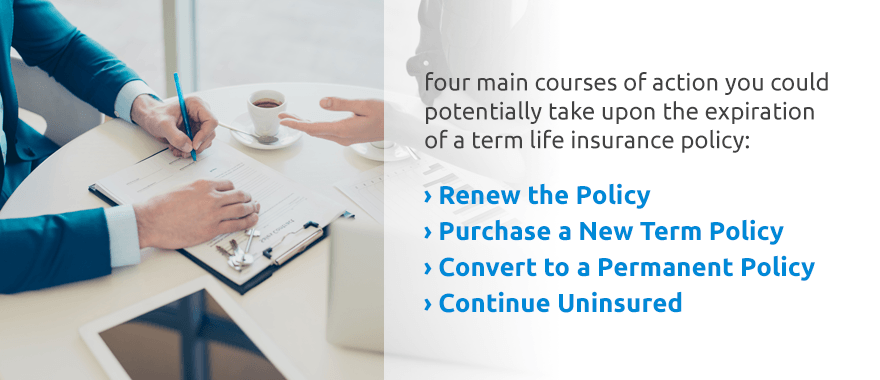

Term life insurance policies can be purchased in a variety of term-lengths, ranging from just one year to 30 years, and in some cases, it can last to a specified age, which tends to be 65. Whatever the term length, when the term runs out, your policy automatically expires. What happens next depends on the policy type you had and your need going forward. There are four main courses of action you could potentially take upon the expiration of a term life insurance policy:

If you’re considering term life insurance, here are the main pros and cons to take into account:

Pros

Cons

Annuities are quite different from other types of life insurance policies, but they are another viable financial product to consider. Essentially, annuities are a type of investment contract, so they don’t require the same qualifications that life insurance policies do, but they deliver similar benefits. Annuities are primarily designed to offer you financial benefits if you end up living a long life, but they can also offer a death benefit to your beneficiaries.

To put it another way, while life insurance policies are only designed to protect your dependents from the financial consequences of an untimely death, an annuity also protects against the financial consequences of outliving your financial assets. For this reason, annuities are typically purchased by older individuals.

Essentially, here is how an annuity works. You pay into the annuity over time, and your funds earn a rate of return, tax-deferred, based on either a variable or fixed interest rate. If you outlive your income or retirement funds, you can rely on your annuity to provide you and any dependents with ongoing funds, almost like an income, either for a set amount of time or for as long as you live. In the event of your death, your beneficiaries would receive payments from the annuity. The death benefit your beneficiary or beneficiaries receive can either be distributed across years or paid in one lump sum.

As with all insurance policies, the exact terms of your annuity will depend on the contract you develop with your insurance company. You must be sure to specify any dependents that you wish to inherit your annuity to ensure they will receive the death benefit.

Here are a few pros and cons to think through if you’re considering purchasing an annuity instead of more traditional forms of life insurance:

Pros

Cons

To qualify for life insurance, you will have to demonstrate to the insurance company that you can afford it and that you are not a high-risk candidate. In every case, you will start by filling out an application. This application will ask for basic information, such as your name, height and weight, as well as more detailed information about your lifestyle, personal health history and family’s health history.

For some insurance companies, you may also be required to undergo a physical examination. This exam is intended to establish a more complete picture of your current health. It may include basic height, weight and blood pressure checks as well as lab tests of your blood or urine. In some cases, you may be asked to participate in extra tests, such as a chest X-ray or a treadmill test.

So, what are insurance companies looking for your application or medical exam? They want to establish that you do not have any significant health issues that may impact your potential life expectancy. It may sound morbid, but that’s just how insurance works. You are making an investment, and so is the insurance company. The ideal situation for both the insurance company and for you and your family is that you won’t ever need to take advantage of your insurance’s benefit.

If you do have health conditions or aspects of your occupation that make you a more high-risk candidate for the life insurance company, they may deny you coverage or offer you a policy with higher premiums.

Here are some examples of things that could either disqualify you for life insurance or result in a higher life insurance cost:

Even if one insurance company says you don’t qualify for a life insurance policy, that doesn’t necessarily mean you can’t find coverage anywhere. Each insurance company is different, so it’s smart to seek coverage elsewhere before giving up.

If you live near Washington, Union or St. Clair, Missouri and are looking for the right life insurance brokers to provide you with the expert guidance you need to choose the best policy for you at a rate you can afford, consider David Pope Insurance Services, LLC. We understand how important it is that you find the perfect balance of coverage you can afford and that will give you the comprehensive coverage you need to know your family will be financially secure.

With over 20 years of experience and more than 15 years in the business, David Pope Insurance Services, LLC has the expertise and established relationships necessary to help you find the perfect policy for you. We understand that each family is different, and we want to meet your specific needs. We won’t stop until we’ve found the best possible solution for you.

We also understand that trying to determine what type of life insurance coverage you need can be a stressful task, especially when you try to figure it out on your own. When you speak to one of our agents, you’ll experience the care that can only come from a local, family-owned and operated business. We understand and care about Missourians.

Our agents are extremely knowledgeable in the options available and can provide you with quotes and policies to meet your unique financial situations and needs. It’s what we do every single day. If you’re afraid you won’t be able to afford life insurance, don’t let that keep you from reaching out for more information. Based on our years of experience, we can assure you that it is possible to find affordable policies that meet your needs. We know the best ways to make your insurance affordable, like identifying bundling discounts to drive down your premium cost.

We’re ready and eager to help you find the perfect life insurance policy for you and your family in Missouri, Arkansas, Iowa, or Kansas. Call us at 636-583-0800 or contact us today for life insurance quotes online. Our quotes are fast, free and accurate. Speaking to an agent is a great way to get your questions answered, help you decide whether life insurance is a smart move for you and choose what type of policy you should invest in. We want to help you stay within your budget while enjoying peace of mind knowing that the people you love most will be well-cared for, no matter what.