Many people only think about insurance once they need to use it. However, you might be paying more than necessary for the coverage you’re receiving. Insurance rates have continued to increase over time. Experts estimate that car insurance rates will increase by 8% in 2023 alone.

Luckily, higher rates don’t necessarily mean you have to pay too much for car insurance. Regularly checking your coverage, knowing what factors affect the premiums you pay and adjusting your policies will help you avoid excessive costs.

Jump To:

A variety of factors affect how much you pay for home insurance or auto insurance. Some of these are beyond your control, while others you can adjust or correct as needed. Understanding everything that comprises your insurance cost of your insurance will help make you a better-informed consumer. Knowing what influences your rates can also help you as you shop around for a new insurance policy.

Although you can’t receive preferential treatment based on your gender or age in many areas of life, insurance isn’t one of them. Insurers, particularly those offering car insurance, can adjust your rate based on how old you are or your gender, at least in some states.

Here are some ways that gender and age can impact your insurance costs:

Your driving history also impacts your insurance rates. If you drive recklessly or have a history of many speeding tickets or accidents, your insurance premiums should be higher than someone who has a clean driving record.

The number of years you’ve driven also affects your insurance. If you’re new to being behind the wheel, your driving record is relatively untested. An insurance company is taking a more significant chance on you compared to someone who has driven for years without so much as a speeding ticket or getting into a fender bender. The longer your driving record, the lower your insurance rates can become.

The same is true of how long you’ve been driving. If you’re new to being behind the wheel, your driving record is relatively untested. An insurance company is taking a more significant chance on you compared to someone who’s been driving for years, without so much as a speeding ticket or fender bender.

Another factor influencing your insurance rates is why and how often you use your car. If you drive for work, you might have to pay a higher premium compared to someone who only drives for personal reasons or who rarely gets behind the wheel.

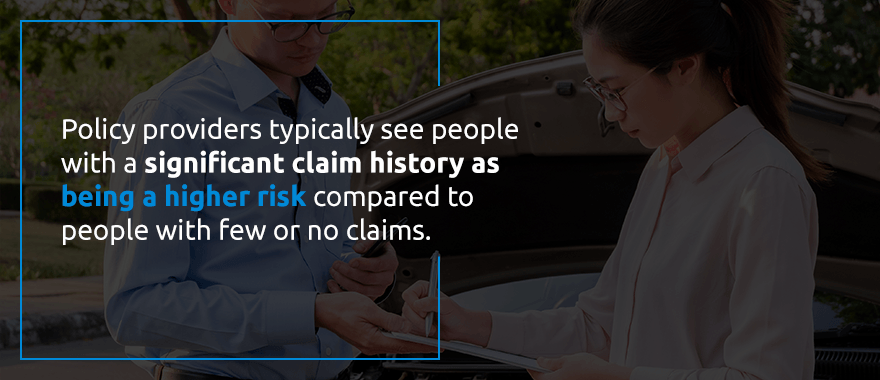

The goal of having insurance is to have protection if you get into an accident. The more you need to use your insurance protection, the more you cost insurance companies. Policy providers typically see people with a significant claim history as being a higher risk compared to people with few or no claims. That’s one of the reasons your insurance premiums typically rise after you have a car accident or otherwise need to use your insurance coverage.

Your claim history also influences the rates you pay for home insurance. Any claims filed on the home during the past seven years go into the Comprehensive Loss Underwriting Exchange (CLUE) database. Insurers look at a home’s or car’s CLUE report to see if there has been a history of claims and to get a better sense of what those claims were.

While you can’t change your past, you can take steps to minimize future claim numbers. In turn, you can keep your rates lower.

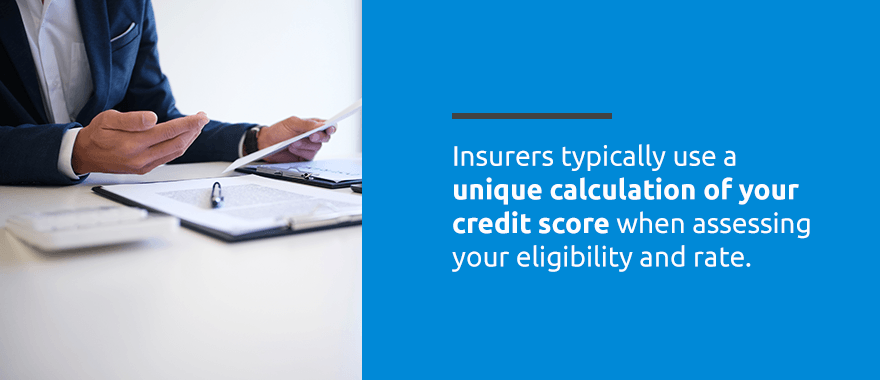

Your credit score does much more than determine whether you’re eligible for a loan or the interest rate a lender will offer you. It can also influence your insurance premiums, particularly for car insurance. Insurers typically use a unique calculation of your credit score when assessing your eligibility and rate. It’s not the same score a lender uses when approving you for a loan. That said, many of the same factors, such as your payment history and the amount of debt you have, go into determining your car insurance credit score.

If you’re concerned about how your credit history affects your insurance rates, focus on reducing your total debt amount, stay updated on your payments and bring down your credit use ratio.

Your location also affects home and car insurance. In the case of home insurance, you will likely pay more for your premiums in an area with a higher-than-average number of natural disasters. If you live in an area that experiences flooding, you’ll most likely need to pay extra to purchase flood insurance, for example.

Living in a city or densely populated area can mean higher car insurance rates. A large city can mean a greater number of cars and a higher risk of a collision or another accident. Some areas also have higher rates of theft, which can drive up your insurance rates for homes and cars. One way to lower these rates is to purchase anti-theft tools, such as a car alarm or home security system.

Your home’s condition also influences your rates. Recently built homes are often less expensive to insure compared to older ones. In addition, homes often cost less when they consist of more durable materials like brick.

Your vehicle type can also impact your car insurance costs. For instance, providers will consider factors like:

Another factor influencing your insurance rates is why and how often you use your car. The more often you drive, the more opportunities you have to get into accidents. If you drive for work, you might have to pay a higher premium compared to someone who only drives for personal reasons or who rarely gets behind the wheel.

Insurance providers typically ask for annual mileage while they process your claim. That way, they can assess your average usage and adjust your claim as needed.

No one wants to pay more than necessary for their insurance. While you can’t control some of the factors that affect your rates, like your age or gender, you can use various methods to avoid paying too much for insurance. If a lot of time has passed since you viewed your insurance rate or browsed for a new policy, you might realize you’re overpaying for car insurance coverage you don’t need. Additionally, major life changes can impact your policy costs. For instance, getting married or turning 25 can affect your premiums. It’s always best to monitor your insurance policies to make sure you’re not paying too much.

It’s a good idea to check in on your insurance from time to time to make sure it still meets your needs. If many years have passed since you last looked at your insurance policies, you might be paying for coverage you don’t need.

Here are some strategies for how to not overpay for car insurance:

If you’re driving an older car, you might not need to insure it for as much as you did when the car was new or when you were still paying off your car loan. You may find you can benefit from less coverage and a lower premium.

Alternatively, you might discover you have a low deductible and that switching to a policy with a higher deductible helps you save a considerable amount. A higher deductible will mean you need to pay more out of pocket if there’s a problem with your home or car, but it also means you spend less upfront.

It’s also worthwhile to check to see if you’re eligible for discounts on your insurance premium. Many auto insurance policies offer discounts, ranging from a reduced premium for drivers who haven’t had a claim in several years to lowered premiums for people who complete a driver’s education course. Bundling insurance policies, such as combining your home and auto insurance, can help reduce your rate, too.

You might also want to ask about the factors that are affecting your premiums. If you’re driving a small, older car and paying a lot to insure the vehicle, it might be financially worthwhile to purchase a newer car or upgrade to a larger vehicle with more safety features.

It pays to shop around when it comes to insurance, but many people don’t do so. They buy a policy when they become homeowners or when they first get their car, and they keep it until they move or get a new vehicle. If it’s been some time since you looked at policies, it’s a good idea to ask your insurance broker to show you what’s available. An insurance broker works with you to help you find the best policy at the best rate. They don’t represent one single insurance company, meaning they are working for you to identify a policy that is in your best interests and that matches your current needs.

Perhaps you’ve been overpaying for your auto insurance and your current policy no longer meets your needs. The same is true for your home insurance. With the support of an insurance broker, you can pick a policy that provides the coverage you need for a lower overall premium.

It’s also a good idea to browse average insurance costs are for your city, town or neighborhood you live in. Location matters when it comes to insurance premiums for car and home insurance. Areas with low rates of crime are likely to have lower premiums compared to areas with high theft rates. The same is true for areas that experience extreme weather events, compared to ones that don’t.

Request a Free Homeowners Insurance Quote

Along with getting a sense of the average cost of insurance in your area, it’s worthwhile to research how you can do to reduce that cost. For example, if you live in a city and own a car, you might get a discount on your insurance premium if you pay to park your car in a garage or other secure parking area, rather than parking it on the street. In the case of home insurance, your premiums might drop if you invest in storm-resistant roofing materials, storm shutters or other improvements that can protect your home from damage due to a natural disaster.

If you currently live in an area with higher-than-average insurance costs, it might make financial sense to relocate. Even a small change, such as moving to the next town over, might be enough to significantly lower your insurance premiums. Once you know what insurance costs are for the area, you can weigh the pros and cons of relocating.

To shop for insurance discounts, it’s helpful to first understand which discounts providers commonly offer. Discounts you may be eligible for include:

Ask your insurance provider about what discounts may be available to you to make sure you’re getting the most out of your policy for the most affordable price.

Besides discounts, there are a few other options you may have for lowering your insurance costs.

Pursuing these strategies can help you to not overpay for car insurance.

Request a Free Auto Insurance Quote

Several questions for your insurance broker can help ensure you get the coverage you need at a price that works for you. When shopping for insurance, it’s essential to ask the following.

Insurance rates typically increase annually, but that doesn’t mean you are necessarily stuck paying higher and higher premiums as the years go on. If it has been several years since you last shopped for insurance, it can be a good idea to jump back in and shop around for a new policy.

Since time is money and it takes time to shop around for home, renter’s or auto insurance, it can be a good idea to work with an insurance broker. A broker will take your information — such as your age, marital status and gender — and details about your home and car and get several quotes from multiple insurance companies. They’ll show the quotes to you, explain what each one offers and its price and let you pick the policy that seems like the best fit for you.

There’s no need to pay extra for coverage you don’t need. At the same time, you also want to be sure your policy adequately covers your needs. If you’re wondering whether you’re overpaying for insurance, here are some aspects to consider:

If it’s been a while since you shopped for car or home insurance in Missouri, David Pope Insurance is here to help you. Since 2005, many people in Union, St. Clair and Washington have made us their one-stop shop for all their insurance needs. We’ll listen to what you need and help you find an insurance policy that fits your budget, while providing the right amount of protection. Contact us today for quotes and to get started.