Natural disasters such as floods, hurricanes, earthquakes and wildfires can wreak havoc on vehicles, causing damage that can be expensive to repair or even total the vehicle. For this reason, many drivers wonder if their auto insurance policy covers damages caused by natural disasters.

Below, we will explore whether auto insurance covers natural disasters, whether you may want full coverage and how to file a claim after a natural disaster.

Does Car Insurance Cover Natural Disasters?

Car insurance will cover damage from natural disasters if you have comprehensive coverage. Comprehensive coverage is the type of auto insurance that typically covers damages to your vehicle caused by events that are beyond your control, such as natural disasters. This coverage may include damage caused by floods, hurricanes, earthquakes and wildfires.

Note that not all types of auto insurance coverage may cover damages caused by natural disasters. Collision coverage, for example, is another optional type of auto insurance that covers damages to your vehicle caused by a collision with another vehicle or object but typically does not cover damages caused by natural disasters. Liability coverage, which is mandatory in most states and covers damages you may cause to other people’s vehicles or property, also does not typically cover damages caused by natural disasters to your own vehicle.

You want to understand the specific coverage provided by your auto insurance policy and speak with your insurance provider if you have any questions about what is covered. If you live in an area at greater risk of natural disasters, it’s also a good idea to consider additional coverage options to ensure you are fully protected in case of a natural disaster.

When Will Car Insurance Not Cover Natural Disasters?

While car insurance may cover certain natural disasters, there are some situations where coverage may not apply. Here are some examples:

Lack of coverage: If you only have liability coverage, which covers damages or injuries you may cause to other people or property while driving, your insurance policy likely will not cover damages to your own vehicle from a natural disaster.

Failure to purchase comprehensive coverage: Comprehensive coverage, which covers damages to your vehicle from noncollision events like theft, vandalism and natural disasters, is optional in many cases. If you did not purchase comprehensive coverage, your policy likely will not cover damages to your vehicle from a natural disaster.

Exclusions: Your car insurance policy may have exclusions that specifically exclude coverage for certain types of natural disasters. For example, some policies may exclude coverage for floods or earthquakes.

Failure to file a claim in a timely manner: Claims should be filed as soon as possible after a natural disaster occurs. If you wait too long to file a claim, your insurance company may deny coverage.

Fraudulent activity: Coverage may be denied if the insurance company determines that you have submitted a fraudulent claim.

Carefully review your car insurance policy and talk to your insurance provider to understand what is and isn’t covered in the event of a natural disaster.

What Is Full Coverage And What Does It Cover?

Full coverage is a term often used to describe a combination of different types of car insurance coverage that provide a higher level of protection for your vehicle. However, there is no single policy called full coverage that you can purchase.

Instead, full coverage typically refers to a combination of collision coverage, comprehensive coverage and liability coverage. Here’s what each of these types of coverage includes:

Collision coverage: This coverage is optional and covers damages to your vehicle caused by a collision with another vehicle or object. This coverage typically pays for repairs to your vehicle or the actual cash value of your vehicle if it is deemed a total loss.

Comprehensive coverage: This coverage is also optional and covers damages to your vehicle caused by events that are beyond your control, such as natural disasters, theft or vandalism. This coverage may also cover damages caused by hitting an animal or a falling object.

Liability coverage: This coverage is mandatory in most states and covers damages you may cause to other people’s vehicles or property. Liability coverage typically includes bodily injury liability and property damage liability.

Note that the specific coverage provided by your auto insurance policy may vary depending on your insurance provider and the state you live in. Additionally, full coverage does not necessarily mean that your policy will cover all possible scenarios. Review your policy and speak with your insurance provider to ensure that you have the coverage you need to protect yourself and your vehicle.

How Is Full Coverage Different From Comprehensive Coverage?

Full coverage is generally understood to refer to a combination of several different types of coverage, including liability, collision and comprehensive coverage. Comprehensive coverage, on the other hand, is a specific type of coverage that pays for damages to your vehicle that are caused by noncollision events.

So while full coverage may include comprehensive coverage, it also includes other types of coverage, such as liability and collision. Comprehensive coverage is specifically for noncollision damage to your vehicle.

How Do You Know If You Need Full Coverage?

Whether you need full coverage depends on various factors, such as your vehicle’s age and value, your driving history and your budget. Here are a few factors to consider when deciding whether or not to purchase full coverage:

Your vehicle’s age and value: If you have a newer or more valuable vehicle, you may want to consider purchasing comprehensive and collision coverage to protect your investment. However, if your vehicle is older or has a lower value, you may be able to save money by opting for liability coverage only.

Your driving history: If you have a history of accidents or moving violations, you may want to consider purchasing full coverage to protect yourself financially in case of an accident. However, you may be less likely to need full coverage if you have a clean driving record.

Your budget: Full coverage typically costs more than liability coverage alone, so you will need to consider your budget when deciding whether or not to purchase it. Keep in mind that the cost of your insurance premiums also depends on factors such as your age, location and the type of vehicle you drive.

Ultimately, the decision of whether or not to purchase full coverage will depend on your individual circumstances and needs. Review your options carefully and speak with your insurance provider to determine the best coverage for you.

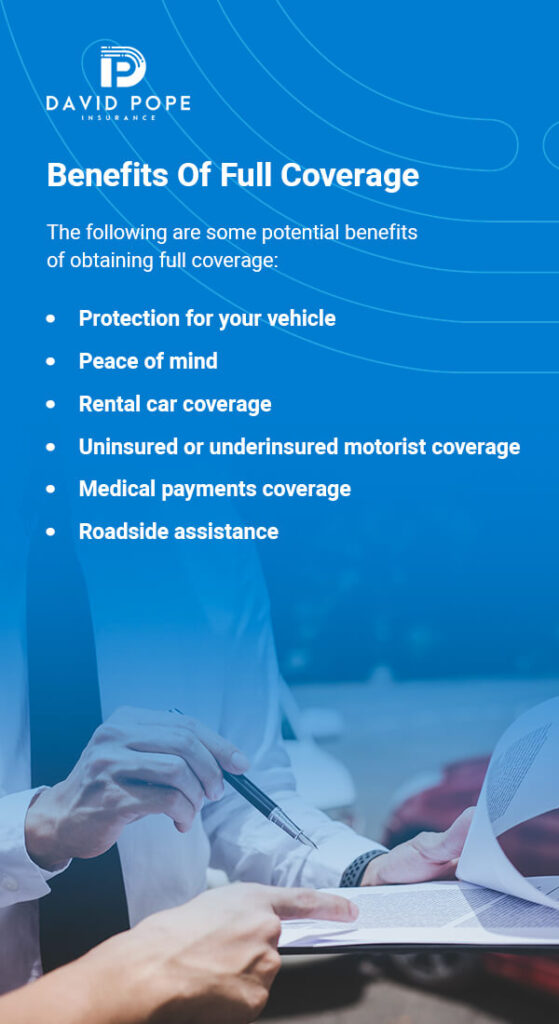

Benefits Of Full Coverage

The following are some potential benefits of obtaining full coverage:

Protection for your vehicle: Full coverage can help protect your vehicle in the event of an accident, theft, vandalism or other covered events.

Peace of mind: Full coverage can provide you with peace of mind and assurance that you have the protection you need in case of an accident or other covered event.

Rental car coverage: Some full coverage policies may include rental car coverage, which can help pay for a rental car while your vehicle is being repaired following an accident.

Uninsured or underinsured motorist coverage: Full coverage policies may also include uninsured or underinsured motorist coverage, which can help pay for damages and injuries if you are in a car accident with a driver without enough insurance coverage.

Medical payments coverage: Medical payments coverage, which is also known as personal injury protection (PIP), may be included in full coverage policies. This coverage can help pay for medical expenses and lost wages for you and your passengers in the event of a car crash, regardless of who is at fault.

Roadside assistance: Some full coverage policies may also include roadside assistance coverage, which can help with services like towing, jump-starts and flat tire changes.

The benefits of full coverage can vary depending on the insurance company, policy and state. Be sure to carefully review your policy to understand what specific benefits are included in your coverage.

How Do You Know If You Have Full Coverage?

If you’re unsure whether you have full coverage, the best way to find out is to review your auto insurance policy or contact your insurance provider directly.

Your auto insurance policy should provide a detailed breakdown of your coverage types and the limits of each coverage. You should be able to find information about your coverage amounts and deductibles, as well as any optional coverages you may have added to your policy, such as comprehensive or collision coverage.

If you’re still unsure about your coverage or have questions about your policy, you can contact your insurance provider directly to speak with a representative. They should be able to provide you with detailed information about your policy and answer any questions you may have.

What Is Considered A Natural Disaster For Insurance Purposes?

For insurance purposes, a natural disaster is typically defined as a catastrophic event caused by natural forces, such as weather or geologic activity. Natural disasters can vary depending on the region and the insurance policy, but they generally include the following:

Severe weather events: This can include hurricanes, tornadoes, thunderstorms, hailstorms, blizzards and floods.

Geologic events: This can include earthquakes, volcanic eruptions and landslides.

Wildfires: This can include wildfires that are caused by natural events, such as lightning strikes or dry conditions.

Other events: This can include other natural events, such as sinkholes or tsunamis.

Keep in mind that not all insurance policies cover all types of natural disasters. For example, some policies may exclude coverage for earthquakes or floods, while others may require you to purchase additional coverage for these events.

How Do You File A Claim After A Natural Disaster?

If you need to file a claim after a natural disaster, here are some steps you can follow:

Contact your insurance provider: The first step is to contact your insurance provider as soon as possible after the disaster occurs. Be prepared to provide your policy number, a description of the damage and any relevant photos or documentation.

Document the damage: Take photos or videos of the damage to your property and belongings. Make a list of any items that were damaged or destroyed.

Mitigate further damage: Take reasonable steps to prevent further damage to your vehicle. This may include covering broken windows, tarping a damaged roof or removing debris.

Meet with an adjuster: Your insurance provider may recruit an adjuster to assess the damage and estimate the cost of repairs. Be sure to provide the adjuster with any documentation or photos you have collected.

Review your policy: Review your insurance policy to understand what is covered and what your deductible is. Your insurance provider can help you understand your coverage and explain the claims process.

File your claim: Once you have gathered all the necessary information, you can file your claim with your insurance provider. Be sure to keep track of all communication with your insurance provider and any paperwork related to your claim.

Act fast after a natural disaster to ensure that your claim is processed as quickly and smoothly as possible. Be patient, as the claims process may take some time, especially if the disaster has affected a large area. If you have any questions or concerns about the claims process, contact your insurance provider for assistance.

How To Choose Coverage

Choosing the right auto insurance coverage can be a complex and overwhelming process. Here are some steps to help you choose the right coverage for your needs:

Understand your state’s insurance requirements: Auto insurance requirements can vary by state, so it’s important to understand what your state requires in terms of coverage. Many states require liability coverage, which covers damages or injuries you may cause to other property or people while driving.

Consider your driving habits and needs: When choosing auto insurance coverage, consider your driving habits and needs. If you have a long commute or frequently drive on highways, you may want to consider additional coverage options like comprehensive or collision coverage. On the other hand, if you only drive occasionally, you may be able to get by with just liability coverage.

Evaluate your budget: Consider your budget when choosing auto insurance coverage. While full coverage may provide more comprehensive protection, it can also be more expensive. Consider your monthly budget and how much you can afford to pay in premiums.

Compare quotes: Shop around and compare quotes from different insurance providers. Make sure each quote includes the same types and amounts of coverage. Beyond the cost, consider the reputation and financial stability of the insurance provider as well.

Review the policy: Once you’ve selected an insurance provider, review the policy carefully. Make sure you understand what is covered and what isn’t, as well as any deductibles or limitations. Ask questions if anything is unclear.

Choosing the right auto insurance coverage can be a time-consuming process, but it’s important to take the time to make an informed decision. By understanding your needs, evaluating your budget and shopping around, you can find the right coverage to protect you and your vehicle.

FAQs

Below are some frequently asked questions about auto insurance and natural disasters.

Do I Need Comprehensive Coverage?

Whether you need comprehensive coverage depends on a number of factors, including the age and value of your vehicle, your driving habits and your overall risk tolerance. Here are some things to consider:

Vehicle age and value: If you have a newer vehicle or one worth a significant amount of money, you may want to consider adding comprehensive coverage to your auto insurance policy to help protect your investment.

Risk of noncollision events: If you live in an area with a higher risk of natural disasters, theft or vandalism, you may want to consider comprehensive coverage to help protect your vehicle in the event of these types of noncollision events.

Your driving habits: If you frequently park your car on the street or in a high-crime area, you may want to consider comprehensive coverage to help protect your vehicle from theft or vandalism.

Your risk tolerance: If you have a low tolerance for risk or want the peace of mind that comes with knowing that your vehicle is protected in the event of a noncollision event, you may want to consider adding comprehensive coverage to your auto insurance policy.

Ultimately, whether you need comprehensive coverage is a personal decision that depends on your circumstances. Some lenders may require it if you’re taking out an auto loan. Be sure to carefully review your options and speak with your insurance provider to determine what type of coverage is best for you.

Will My Auto Insurance Premium Go Up After A Natural Disaster?

Whether or not your auto insurance premium will go up after a natural disaster depends on a number of factors, including the severity of the disaster, the number of claims filed in your area and your individual policy.

In general, if you file a claim for damage to your vehicle caused by a natural disaster, your insurance company may view you as a higher risk, which could increase your premium. However, not all insurance companies will raise rates after a natural disaster, and some may have specific policies in place to prevent rate increases in these situations.

If you are concerned about the possibility of a rate increase after a natural disaster, it’s a good idea to prepare by speaking with your insurance provider to understand their specific policies and procedures. Consider shopping around for insurance quotes to find a policy that offers the coverage you need at a competitive rate.

In some cases, your insurance premium may go up due to factors outside of your control, such as changes in state laws or an increase in overall claims in your area. In these situations, working with an experienced insurance agent who can help you navigate the changing insurance landscape and find the best coverage options for your needs may be helpful.

Reputation: A reputable insurance provider like David Pope Insurance can offer peace of mind and assurance that your claims will be handled fairly and efficiently.

Coverage options: We offer a range of coverage options to meet your needs, including liability, collision and comprehensive coverage. This ensures you have the protection you need in case of an accident or other covered event.

Personalized service: We offer personalized service and take the time to understand your unique needs and circumstances. This can help ensure that you get the right coverage for you.

Bundling discounts: If you also need home or other types of insurance, bundling your policies with us may lead to discounted rates.