When you have to contend with car payments and fuel costs, one of your top priorities should be to learn how to lower your car insurance premiums. Here you will learn more than 20 things that make car insurance cheaper, with advice on:

Get the cheapest car insurance rates possible with us and get a free quote.

Additionally, information on auto insurance tracking devices, as well as tips on how to get cheap car insurance at 18, are covered in the following sections. So, you do get the cheapest car insurance possible?

More Auto Insurance How-To Guides:

Certain companies have been found to offer higher rates to individual drivers based on predictive modeling, where a search into the applicant’s record indicates that he or she would be unlikely to change insurance providers. Fortunately, this tactic – typically referred to as “price optimization” – has been outlawed in 16 states.

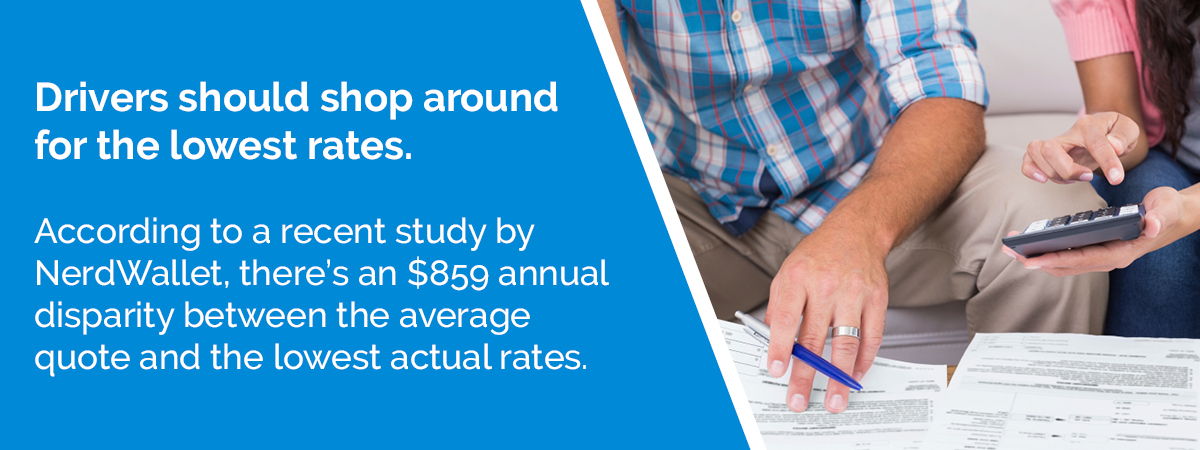

In any case, drivers should shop around for the lowest insurance rates. According to a recent study by NerdWallet, there’s an $859 annual disparity between the average quote and the lowest actual rates.

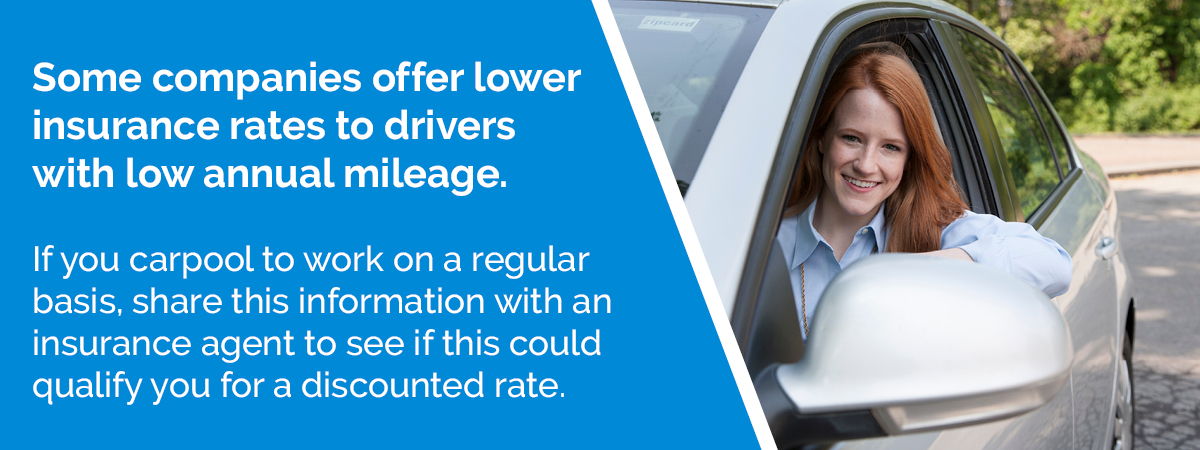

A lot of companies offer lower insurance rates to drivers with low annual mileage. If you only commute short distances to and from work, or if you carpool to work on a regular basis, share this information with an insurance agent to see if this could qualify you for a discounted rate. Some carriers will also offer discounts to applicants that opt for paperless billing, as this saves companies on overhead expenses.

Insurance companies are also known to offer discounts to veterans and members of select professions, including teachers and engineers. To find out if you qualify, ask each agent you speak with for a list of which groups receive such discounts if any.

Discounts are also often given to senior citizens and drivers of vehicle with anti-theft and high-tech safety features. Even if you’re under age 25, you can score a lower rate if you belong to a student honors program.

A word of warning – don’t confuse discounts for low rates. Some companies that offer significant discounts often charge higher than average insurance rates. As such, you’d still be paying more than most drivers for your insurance even after your monthly subtracts all the discounts.

than that of a Honda CR-V.If you’ve settled on a shortlist of prospective cars for your next vehicle purchase, contact your insurance company to check the going insurance rate for each car. This way, you could end up netting huge savings on the overall costs of owning a vehicle.

than that of a Honda CR-V.If you’ve settled on a shortlist of prospective cars for your next vehicle purchase, contact your insurance company to check the going insurance rate for each car. This way, you could end up netting huge savings on the overall costs of owning a vehicle.

To select an insurance policy that best suits your needs as a driver, you need to your own vehicle. As long as you lease a car, your insurance policy is chosen by the leasing entity, not you. In these arrangements, insurance policies are often expensive.When a leasing entity entrusts you with their vehicle, they’ll usually require that you have the most comprehensive insurance policy to ensure that no money gets taken out of their pocket in the event of an accident. Simply put, if you don’t own the car that you drive, you don’t get to choose the insurance policy.If you skip the lease and secure a loan, you’ll still pay more for your insurance. Once again, the bank will own the car, which will require you to have the most comprehensive insurance policy available. Furthermore, by the time you’ve paid off such a loan, you’ll have paid a greater total amount than what the vehicle was ever worth. In the long run, there’s no money to be saved by leasing or getting a loan on a car.

To select an insurance policy that best suits your needs as a driver, you need to your own vehicle. As long as you lease a car, your insurance policy is chosen by the leasing entity, not you. In these arrangements, insurance policies are often expensive.When a leasing entity entrusts you with their vehicle, they’ll usually require that you have the most comprehensive insurance policy to ensure that no money gets taken out of their pocket in the event of an accident. Simply put, if you don’t own the car that you drive, you don’t get to choose the insurance policy.If you skip the lease and secure a loan, you’ll still pay more for your insurance. Once again, the bank will own the car, which will require you to have the most comprehensive insurance policy available. Furthermore, by the time you’ve paid off such a loan, you’ll have paid a greater total amount than what the vehicle was ever worth. In the long run, there’s no money to be saved by leasing or getting a loan on a car.

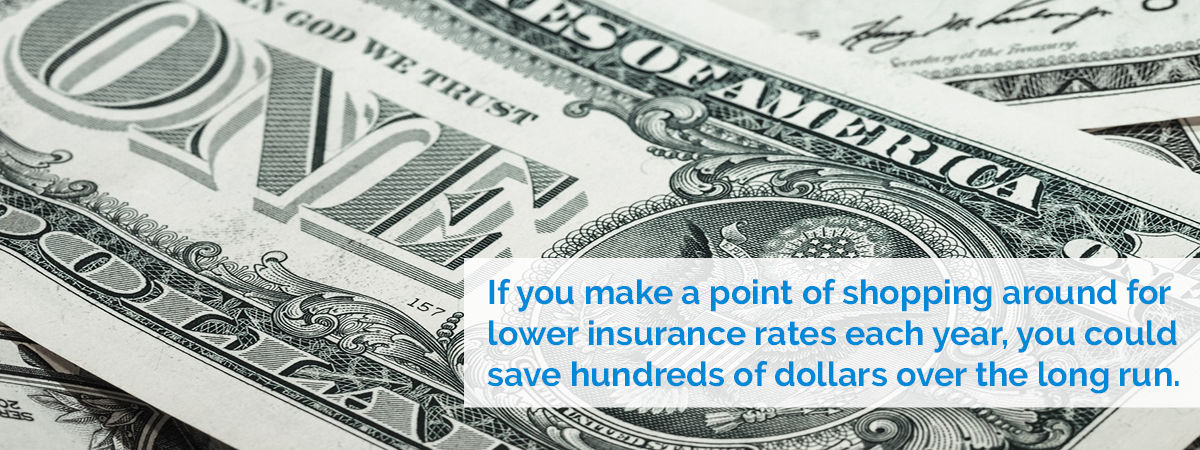

Mark your calendar once per year to compare three of the best insurance quotes offered in your area.

The last of those points were particularly important. In the minds of insurance carriers, one of the greatest predictors of responsible driving is when a driver brings a child into a vehicle. A domestic partnership could also qualify you for a lower rate.

While it’s true that homeownership is beyond the means of many drivers, insurance companies often view homeowners more favorably among incoming pools of applicants.

If you get ticketed for speeding, one of the easiest ways to avoid a rise in your insurance premiums is to change carriers. Likewise, a minor accident liability could signal that it’s time to change policies. On the upside, a ticket or accident fine could serve as a motivating factor in your annual search for a new policy.

If you haven’t been ticked yet, but wish to avoid premium hikes in the event of a speeding or collision fine, ask your insurance provider whether you can include a forgiveness clause in your policy. As long as you prove yourself as a safe, cautious driver overall, some carriers – knowing that most drivers get into accidents or get cited for speeding at some point – will forgive you for the first such incident. Just do your best to notice speed signs and pay attention to your speed meter as you drive.

As with fines for accidents, first-time speeding tickets are likelier to be forgiven by insurance carriers if you submit to a safe driving course. When you show this level of commitment, it sends the message to carriers that you’re not a reckless driver. There are multiple driver discounts provided as a way to make your car insurance affordable.

A word of warning about collision liability – never assume that the other party forgot the incident. Report collisions to your carrier immediately, no matter how minor or seemingly benign. You might think that the other party will brush things off, only to get slapped with a court order months later. This gives your insurance company no time to prepare for your defense and renders you irresponsible and untrustworthy in the eyes of the carrier.

With more than 20 years of experience in the Missouri Insurance Industry, David Pope Insurance has helped drivers from all walks of life secure affordable rates on their car insurance. If you live in Missouri, Iowa, Arkansas, or Kansas, contact David Pope Insurance agents to request a low rate on your next car insurance policy.